Tweet

Tweet

Re: The Elusive Canadian Housing Bubble

THE CANADIAN HOUSING MARKET � IN CHARTS

1) Canada�s housing market is 63% overvalued relative to its historical average�

2) Home prices in Vancouver are more expensive than they are in Sydney, London, and New York�

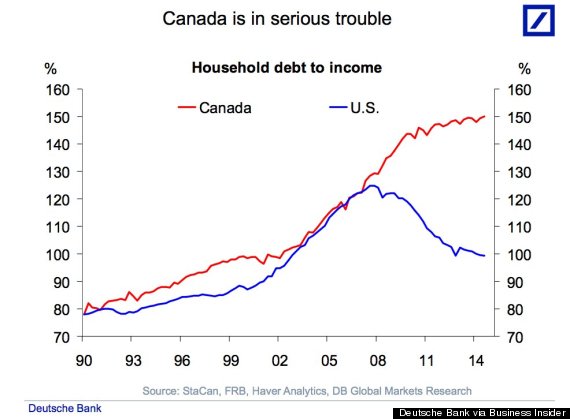

3) �Canada is in serious trouble� because its households never deleveraged�

4) Since 2000, growth in assets held by Canadian banks is as follows�

Personal lines of credit: + ~650%

Credit card loans: + ~400%

Mortgages: + ~250%

Disposable income: + ~100%

5) In Canada, multifamily construction is at record highs�

6) Canadian workers are twice as reliant on housing construction�

In conclusion�

� The Canadian housing market is very expensive.

� Median house price to median household income is higher in Vancouver than it is in Sydney, London, and New York.

� Canadian households � unlike their US counterparts � never deleveraged after the financial crisis.

� Credit is growing a lot faster than income is.

� There�s a lot of supply coming onto the market.

� The share of Canadian workers in housing construction is twice what it is in the US.

If rates rise or if commodity prices continue to fall then it�s likely that Canada�s housing market will come under pressure.

2) Home prices in Vancouver are more expensive than they are in Sydney, London, and New York�

3) �Canada is in serious trouble� because its households never deleveraged�

4) Since 2000, growth in assets held by Canadian banks is as follows�

Personal lines of credit: + ~650%

Credit card loans: + ~400%

Mortgages: + ~250%

Disposable income: + ~100%

5) In Canada, multifamily construction is at record highs�

6) Canadian workers are twice as reliant on housing construction�

In conclusion�

� The Canadian housing market is very expensive.

� Median house price to median household income is higher in Vancouver than it is in Sydney, London, and New York.

� Canadian households � unlike their US counterparts � never deleveraged after the financial crisis.

� Credit is growing a lot faster than income is.

� There�s a lot of supply coming onto the market.

� The share of Canadian workers in housing construction is twice what it is in the US.

If rates rise or if commodity prices continue to fall then it�s likely that Canada�s housing market will come under pressure.

).

).

Comment