Tweet

Tweet

Re: Vancouver goin'?

[COLOR=rgba(255, 255, 255, 0.870588)]

[/COLOR]

[COLOR=rgba(255, 255, 255, 0.870588)]

[COLOR=rgba(0, 0, 0, 0.541176)]

1 h 20 min without traffic

[/COLOR]

[/COLOR]

1 h 18 min [COLOR=rgba(0, 0, 0, 0.541176)](39.1 km)

[/COLOR]

[COLOR=rgba(0, 0, 0, 0.541176)]via Trans-Canada Hwy/BC-1 E

1 h 20 min without traffic

[/COLOR]

Originally posted by GRG55

View Post

[COLOR=rgba(255, 255, 255, 0.870588)]

[/COLOR]

[COLOR=rgba(255, 255, 255, 0.870588)]

Leave now

[COLOR=rgba(0, 0, 0, 0.541176)]

[COLOR=rgba(0, 0, 0, 0.870588)]1 h 18 min[/COLOR]

39.1 km

via Trans-Canada Hwy/BC-1 E39.1 km

1 h 20 min without traffic

This route includes a ferry.

[/COLOR]

[/COLOR]

1 h 18 min [COLOR=rgba(0, 0, 0, 0.541176)](39.1 km)

[/COLOR]

[COLOR=rgba(0, 0, 0, 0.541176)]via Trans-Canada Hwy/BC-1 E

1 h 20 min without traffic

This route includes a ferry.

[/COLOR]

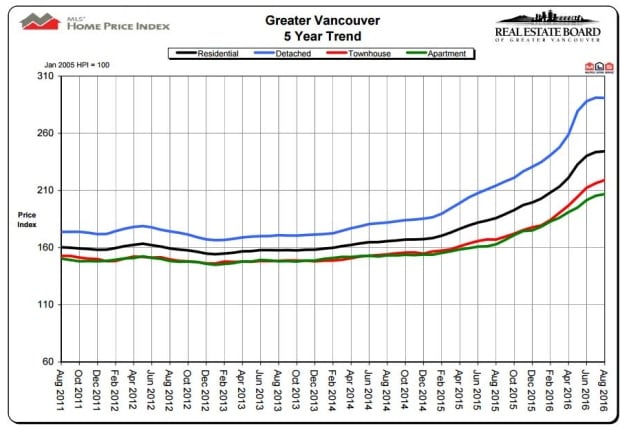

}. They will be among the many that follow the market down, always just behind the curve. FOMO is alive and well and living in the GVRD.

}. They will be among the many that follow the market down, always just behind the curve. FOMO is alive and well and living in the GVRD.

Comment