Tweet

Tweet

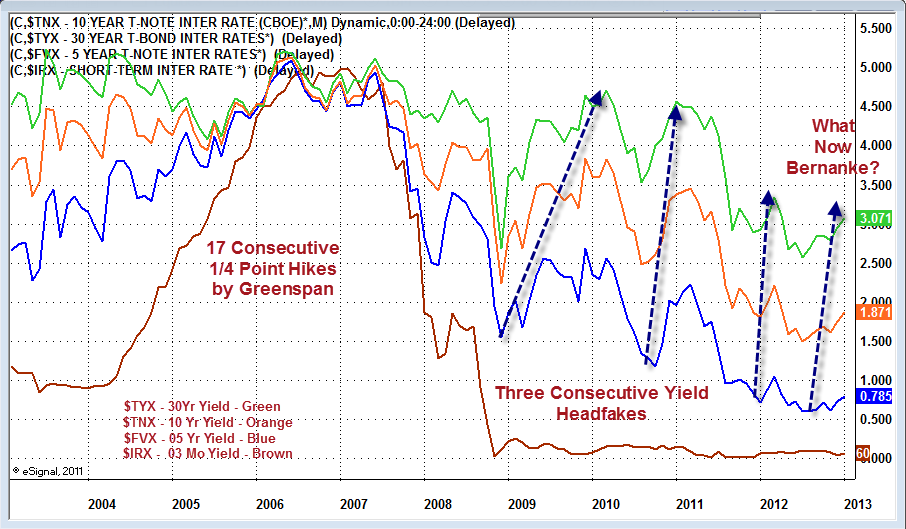

Re: treasury yields

True, but you're not accounting for risk in that analysis. There is a reason why the spreads are high right now. If the banks could risklessly arbitrage that gap back down, it by definition wouldn't be there.

True, but you're not accounting for risk in that analysis. There is a reason why the spreads are high right now. If the banks could risklessly arbitrage that gap back down, it by definition wouldn't be there.

Comment