Tweet

Tweet

| Another captain obvious? Although Roach's been at it for a long time singing the same tune... Good weekend to all and kudos for those with balls to short the market! (Jim are you listening?) -L. Roach: Global Downturn Just Getting Started | ||

| ||

The financial media has put much of its focus recently on how close the credit crisis is to the finish line. Not so fast, says Stephen Roach, chairman of Morgan Stanley Asia. While "credit market contagion is maybe two-thirds behind us, the impact on the U.S. and global economies is at an early stage," he tells Bloomberg TV. The bursting of the housing and credit bubbles and the surge in oil prices have just started to dent U.S. consumers, Roach says. "For the U.S. consumer, where a record 72 percent of GDP was going to personal consumption last year, that share has to come down," he argues. "As it does, the production of global economies will weaken. We are in the early stages of a downturn in the U.S. and global business cycle. It could be a multi-year adjustment for U.S. consumers." The weakness in U.S. consumption and the negative impact that weakness will have on the rest of the world's economies will be the big global economic story for the rest of the year, Roach says. The Federal Reserve's most recent report on economic conditions, known as the Beige Book, backs up Roach's view. "Consumer spending was reported to be slow in most districts, with purchasing concentrated on necessary items and retrenchment in discretionary spending," the report says. This bad economic news will shift the bear market in stocks away from the financial sector and into non-financial sectors, Roach says. "I think the market trades sideways to lower through early 2009 and possibly longer," he says. � 2008 Newsmax. Link: http://moneynews.newsmax.com/streett...04/127777.html | ||

-

-

Re: Stephen Roach: Global Downturn Just Getting Started

permabears in a bear market can only stay in the game by doubling down... more bearish than the bear-o-the-day.Originally posted by LargoWinch View Post

in a bull market they lay low until the shit hits the fan.

then they have a small window go get some attention.

they have to lay low in bull markets.

bulls lay low in bear markets, sniping and biding their time waiting for their moment.

realists got it on all the time... yeh...! -

Once You Get Started . . .

Stephen Roach:

The world economy is in the grips of a dangerous delusion. As the great boom that began in the 1990s gave way to an even greater bust, policymakers resorted to the timeworn tricks of financial engineering in an effort to recapture the magic. In doing so, they turned an unbalanced global economy into the Petri dish of the greatest experiment in the modern history of economic policy. They were convinced that it was a controlled experiment. Nothing could be further from the truth.

The rise and fall of post-World War II Japan heralded what was to come. The growth miracle of an ascendant Japanese economy was premised on an unsustainable suppression of the yen. When Europe and the United States challenged this mercantilist approach with the 1985 Plaza Accord, the Bank of Japan countered with aggressive monetary easing that fueled massive asset and credit bubbles.

The rest is history. The bubbles burst, quickly bringing down Japan�s unbalanced economy. With productivity having deteriorated considerably � a symptom that had been obscured by the bubbles � Japan was unable to engineer a meaningful recovery. In fact, it still struggles with imbalances today, owing to its inability or unwillingness to embrace badly needed structural reforms � the so-called �third arrow� of Prime Minister Shinzo Abe�s economic recovery strategy, known as �Abenomics.�

Despite the abject failure of Japan�s approach, the rest of the world remains committed to using monetary policy to cure structural ailments. The die was cast in the form of a seminal 2002 paper by US Federal Reserve staff economists, which became the blueprint for America�s macroeconomic stabilization policy under Fed Chairs Alan Greenspan and Ben Bernanke.

The paper�s central premise was that Japan�s monetary and fiscal authorities had erred mainly by acting too timidly. Bubbles and structural imbalances were not seen as the problem. Instead, the paper�s authors argued that Japan�s �lost decades� of anemic growth and deflation could have been avoided had policymakers shifted to stimulus more quickly and with far greater force.

If only it were that simple. In fact, the focus on speed and force � the essence of what US economic policymakers now call the �big bazooka� � has prompted an insidious mutation of the Japanese disease. The liquidity injections of quantitative easing (QE) have shifted monetary-policy transmission channels away from interest rates to asset and currency markets. That is considered necessary, of course, because central banks have already pushed benchmark policy rates to the once-dreaded �zero bound.�

But fear not, claim advocates of unconventional monetary policy. What central banks cannot achieve with traditional tools can now be accomplished through the circuitous channels of wealth effects in asset markets or with the competitive edge gained from currency depreciation.

This is where delusion arises. Not only have wealth and currency effects failed to spur meaningful recovery in post-crisis economies; they have also spawned new destabilizing imbalances that threaten to keep the global economy trapped in a continuous series of crises.

Consider the US � the poster child of the new prescription for recovery. Although the Fed expanded its balance sheet from less than $1 trillion in late 2008 to $4.5 trillion by the fall of 2014, nominal GDP increased by only $2.7 trillion. The remaining $900 billion spilled over into financial markets, helping to spur a trebling of the US equity market. Meanwhile, the real economy eked out a decidedly subpar recovery, with real GDP growth holding to a 2.3% trajectory � fully two percentage points below the 4.3% norm of past cycles.

Indeed, notwithstanding the Fed�s massive liquidity injection, the American consumer � who suffered the most during the wrenching balance-sheet recession of 2008-2009 � has not recovered. Real personal consumption expenditures have grown at just 1.4% annually over the last seven years. Unsurprisingly, the wealth effects of monetary easing worked largely for the wealthy, among whom the bulk of equity holdings are concentrated. For the beleaguered middle class, the benefits were negligible.

�It might have been worse,� is the common retort of the counter-factualists. But is that really true? After all, as Joseph Schumpeter famously observed, market-based systems have long had an uncanny knack for self-healing. But this was all but disallowed in the post-crisis era by US government bailouts and the Fed�s manipulation of asset prices.

America�s subpar performance has not stopped others from emulating its policies. On the contrary, Europe has now rushed to initiate QE. Even Japan, the genesis of this tale, has embraced a new and intensive form of QE, reflecting its apparent desire to learn the �lessons� of its own mistakes, as interpreted by the US.

But, beyond the impact that this approach is having on individual economies are broader systemic risks that arise from surging equities and weaker currencies. As the baton of excessive liquidity injections is passed from one central bank to another, the dangers of global asset bubbles and competitive currency devaluations intensify. In the meantime, politicians are lulled into a false sense of complacency that undermines their incentive to confront the structural challenges they face.

What will it take to break this daisy chain? As Chinese Premier Li Keqiang stressed in a recent interview, the answer is a commitment to structural reform � a strategic focus of China�s that, he noted, is not shared by others. For all the handwringing over China�s so-called slowdown, it seems as if its leaders may have a more realistic and constructive assessment of the macroeconomic policy challenge than their counterparts in the more advanced economies.

Policy debates in the US and elsewhere have been turned inside out since the crisis � with potentially devastating consequences. Relying on financial engineering, while avoiding the heavy lifting of structural change, is not a recipe for healthy recovery. On the contrary, it promises more asset bubbles, financial crises, and Japanese-style secular stagnation.

Last edited by don; May 06, 2015, 09:25 AM.Comment

-

Re: One You Get Started . . .

Originally posted by don View PostI'm just curious what people mean, specifically, when they say 'structural reforms'. Is it simply returning monetary policy to historical settings and letting the resulting reverberations play out until 'market equilibrium' (whatever that actually means) is re-established? Remove all distortions to the market and let the chips fall?

I don't think everyone agrees on what the structural reforms really are. The seem mostly to me to be 'get the other guy to clean up his act but leave my mortgage interest deduction alone'.

Comment

-

Re: One You Get Started . . .

You forgot....

- I'm not giving up my pension, but those Wall Streeters make too much dam money...

- I know my kid can't afford a home, but it makes me feel good knowing my house is worth $XXX,XXX because I'm a smart investor.

- Wow, my $401 Balance is up 300% since 2009 because I'm one of the smartest people on the planet....Wall Street guys are paid too much..Comment

-

Re: Stephen Roach: Global Downturn Just Getting Started

When it comes savings instruments that are financial in nature , not something with essential utility like a a pantry full of pickles, everything can't suck at once it would seem. Ever since 2008 what was often commonly expressed was:Originally posted by metalman View Post

real estate was a black hole

the dollar was "toilet paper"

gold was in a bubble

stocks were doomed

and bonds were all junk.

For some reason oil was left out and it is amusing to see lately its the one thing that should not have been.

Now for those who are perma bears on all financial instruments, I suppose in a disaster labor could be such a premium that no financial instrument could hold sway over it such that what ever was saved will have to be turned over to the only plumber left in town. Unless that happens something has to absorb the desire to save, no?Comment

-

Re: One You Get Started . . .

That's a good point in many discussions, jneal3.Originally posted by jneal3 View Post

Often the question can be made more specific by rephrasing it like this:

"Who should take a big pay cut?"Comment

-

Re: Once You Get Started . . .

I think of structural changes more along the lines of the financialization of the economy, outsourcing production, and strip-mining what's left with debt.Comment

-

Re: One You Get Started . . .

The only politically expedient routes are bees, osterizers and slaves.Originally posted by thriftyandboringinohio View PostComment

-

Re: Once You Get Started . . .

Real structural changes can have dramatic results . . . .

by Charles Hugh Smith

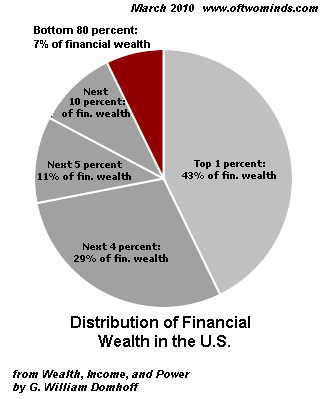

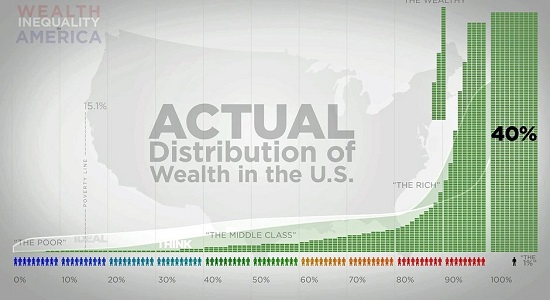

Despite the PR about how corporate profits benefit widows and orphans, this vast wealth is concentrated in the top 1% and the top 5%.

I am honored to share a remarkable data base of Corporate Fines and Settlements from the early 1990s to the present compiled by Jon Morse. Here is Jon�s description of his project to assemble a comprehensive list of all corporate fines and settlements that can be verified by media reports:

�This spreadsheet is all the corporate fines/settlements I�ve been able to find sourced articles about, mostly in the period from the 1990�s up to today (with a few 80�s and 70�s). This is by far the most comprehensive list of such things online. At least that I could find, because the lack of any decent list is what made me start compiling this list in the first place.�

What struck me was the sheer number of corporate violations of laws and regulations�thousands upon thousands, the vast majority of which occurred since corporate profits began their incredible ascent in the early 2000s�and the list of those paying hundreds of millions of dollars in fines and settlements, which reads like a who�s who of Corporate America and Top 100 Global Corporations.

I encourage you to open one of the three alphabetical tabs at the bottom of the spreadsheet on Google Docs and scroll down to find your favorite super-profitable corporation.

Many have a long list of fines and settlements, and many of the fines are in excess of $100 million. Many are for blatant cartel price-fixing, not disclosing the dangers of the company�s heavily promoted medications, destroying documents to thwart an investigation of wrong-doing, etc.

In other words, these were not wrist-slaps for minor oversights of complex regulations� these are blatant violations of core laws of the land.

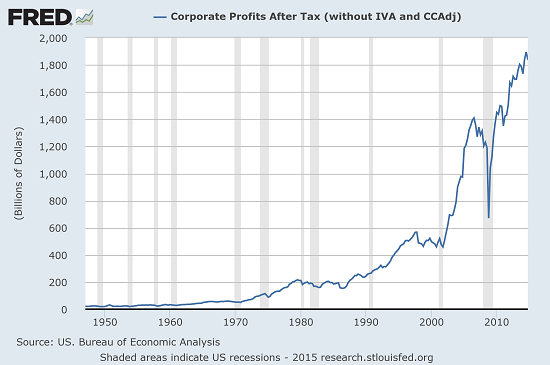

AS you can see in the chart of corporate profits, enormous wealth has been concentrated in the hands of corporate managers and owners since 2002. This alignment with the start of the Federal Reserve�s easy-credit policies is not coincidental.

Despite the PR about how corporate profits benefit widows and orphans, this vast wealth is concentrated in the top 1% and the top 5%:

I asked Jon for his views on the meaning of this mind-boggling list of corporate malfeasance, price-fixing and other wrongdoing in terms of the concentration of wealth: here is his response.

As for the connection to the concentration of wealth: I see two ways in which they are related, the first one is pretty direct and that is the increasing size of the settlements. You will notice that as the settlement date gets later the average size gets much larger. Corporate profits after tax (without IVA and CCAdj) from 1st quarter to 1947 to 4th quarter 2014 went from $21,900,000,000 to $1,837,500,000,000 which is a 8290% increase, even from 1st quarter 1980 to 4th quarter 2014 went from $211,600,000,000 to $1,837,500,000,000 which is a 768% increase.

The second link is less direct. With the increases in concentration of wealth there has been a culture of idolizing wealth, one example is how prosecutors no longer find it appropriate to put banker�s and CEOs in jail. I think one side-effect of the culture changing has been an increased willingness to break the law to increase profits.

The settlements with the banks along with the ongoing investigations have shown that virtually every market is being manipulated; the stocks, metals markets, LIBOR, FOREX, everything. The companies would only break so many laws if they felt they would have a reasonable chance of getting away with it; they would also need a reason to do it, which is provided by the infinite growth model our economy is based on.

Thank you, Jon, for compiling a tremendously important and valuable database of corporate fines and settlements, and for connecting this staggering list of violations to the cultural worship of maximizing private gains at any cost. I am reminded of socio-economist Immanuel Wallerstein�s description of the current world-system of central-state/private-corporation collusion as �a particular historical configuration of markets and state structures where private economic gain by almost any means is the paramount goal and measure of success.�

Wallerstein and four colleagues explored the future of this wealth-concentration/maximizing private gain model in Does Capitalism Have a Future? (Oxford University Press, 2013).

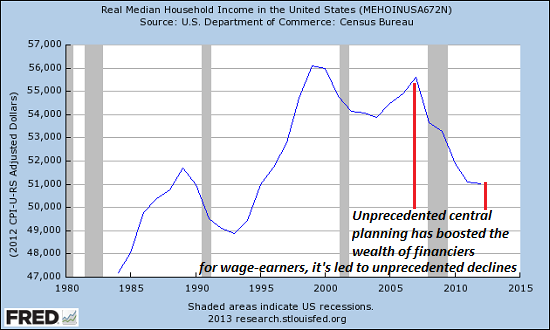

Please consider these charts:

Of related interest:

Is There Capitalism After Cronyism? (August 30, 2014)

For the Love of Money

IN my last year on Wall Street my bonus was $3.6 million � and I was angry because it wasn�t big enough. I was 30 years old, had no children to raise, no debts to pay, no philanthropic goal in mind. I wanted more money for exactly the same reason an alcoholic needs another drink: I was addicted.

Comment

-

Re: One You Get Started . . .

While there are frequently pay cuts and other forms of pain as a result of structural reforms, if the reforms are REALLY structural, these are often either relatively small, or pretty well-justified.Originally posted by thriftyandboringinohio View Post

To illustrate with an example, in Greece, there is no central registration for land ownership, so there is no reliable way to assess property taxes. A structural reform would be something like implementing such a registry, to unambiguously identify title for all parcels of land in the country. Note that this is neither a reduction of government, NOR a privatization (two notable demons of austerity). If anything it increases the size of government, and permits more government oversight of private transactions.

This will certainly result in some people paying more (those who previously dodged their tax bill by owning land but not claiming it on their taxes). And that would certainly result in both higher revenue, and a different spread of the economic burden than is presently imposed. But to say that this boils down to just "who pays more" is more than a little unfair. (It implies that lying on your taxes is a morally and practically valid position for a nation as a whole to encourage.)

If it is possible to reduce a change to a mere list of winners and losers, that change is probably not a structural reform at all. Some institution must in some way be rebuilt into a more sensible form in order for that tag to fit. It is the rebuilding that makes structural reforms worth implementing, not (primarily) the change in the direct costs.

The registry would encourage economic activity, and also provide a more fair and reasonable distribution of the tax burden. It makes sense because the present system is fundamentally irrational, and counterproductive. When "structural reforms" are administered properly, they provide a tremendous boost to an economy.

So while some of the changes being implemented in a given place may or may not actually MEET a rigorous definition of a "structural reform" when they do so, it is generally a good thing for the economy as a whole, even if the imposition of the reform also happens to redistribute wealth.

The problem is that in order to implement real structural reform, one has to challenge a whole lot of entrenched special interests. In the land-registry case, it is actually believed that a majority of Greeks evade their tax bill. Since closing this loophole is therefore unpopular, the government has done everything in its power to claim to be making progress, without actually doing it. Instead it implements changes that are not really structural at all: pay cuts, staff reductions, etc. These may indeed change the economic circumstances somewhat, but since they are only a difference of size and not a difference in kind, they are not actually structural reforms. And often they hurt more than they help.

For this reason, I separate the concept of "structural reform" from mere "austerity". Structural reforms make sense. Austerity for its own sake, does not.

But it is not an accident that it is hard to tell what is really meant by "structural reforms". It is in the interests of a lot of people to ensure that there as much confusion on this question as possible.

One key to the problem is that it will always be in the interests of a popularly elected government to muddle these two terms into incomprehensibility, so that it can claim to be doing something, while dodging the most important, and hence unpopular, real reforms. If it can make voters mad enough about "austerity" without actually implementing a single real reform, then it will have a popular mandate to cast off both austerity and reforms, without ever having to pay the political price associated with making people pay their taxes. It is in the interests of all local elected officials to insist that ANY changes demanded are NOT structural, but rather austerity (cuts).

And without belaboring the point, it should be clear that it is in the interests of the banks who did the lending to insist that ALL of the changes they are demanding are "structural" even when some might in fact be simple budget cuts to improve the odds of payment on debt.

And that's how jneal3's question, and thrifty's reply, really does cut to the very heart of the matter.

It's precisely NOT about "who takes the pay cut?"

It's about "who wants to remain behind a veil of secrecy?" Who is most busy sowing the confusion about the nature of the change? Who is misdirecting the viewer away from the text of what is being done? Who is making public specific language of proposed bills to analyze, and who is talking in generalities and intentions?

In Greece, it's tax-dodgers. In the US its political donors. But make no mistake, every country has some form of structural reform that would benefit it, but is opposed by one or another special interest group, that is powerfully motivated to keep some transaction hidden.

And there's only one reason for that: On some level, they know what they are doing is wrong.

And if it is made public, some force (public pressure, ineffectiveness of the method, etc.) will make them stop.

So the thing to do, if structural reform is to be helpful, is demand radical transparency.

Whoever screams loudest against that is probably your villain.

So to come back to the original question:If the voters of a society have agreed that a mortgage interest deduction is ok, then no one is going to try to hide the fact that they take the deduction. Transparency won't touch that one bit.Originally posted by jneal3 View Post

And being driven to a true "market equilibrium" would similarly be another approach that a society might choose (though none that I know of has chosen that yet).

But what we have now is a system where no one has any idea where the market equilibrium might be, because there are so many hidden fingers on the scales.

"Structural reform" conducted properly, is at its core about shining light on the faces those fingers belong to. And if everyone agrees that those are the right people, then there really isn't going to be any "other guy" to vilify.

But really, how many of us believe that such transparency will serve up no objectively identifiable villains?Comment

-

Re: One You Get Started . . .

structural reform from Hedges...

Corporation after corporation, including banks, energy companies, the health care sector and defense contractors, must be broken up and nationalized. We must institute a nationwide public works program, especially for those under the age of 25, to create conditions for full employment. We must mandate a $15-an-hour minimum wage. We must slash our obscene spending on defense—we spend $610 billion a year, more than four times the outlay of the second-largest military spender, China—and cut the size of our armed forces by more than half. We must rebuild our infrastructure, including mass transit, roads, bridges, schools, libraries and public housing. We must make war on the fossil fuel industry and turn to alternative sources of energy. We must place heavy taxes on the rich, including a special tax on Wall Street speculators that would be used to wipe out the $1.3 trillion in student debt. We must ensure that education at all levels, along with health care, is a free right of all Americans, not something accessible for the wealthy alone. We must abolish the Electoral College and mandate public financing of political campaigns. We must see that the elderly, the disabled, poor single parents and the mentally ill receive a weekly income of at least $600, or we must find them space in state-run institutions if they require daily care. We must institute a moratorium on foreclosures and bank repossessions. We must end our wars and the proxy wars in the Middle East and bring home our soldiers, Marines, airmen and sailors. We must pay reparations to Iraq and Afghanistan, and to African-Americans whose ancestors largely built this country as slaves who never were compensated for their labor. We must repeal the Patriot Act and Section 1021 of the National Defense Authorization Act. We must abolish the death penalty. We must dismantle our system of mass incarceration, release the vast majority of our 2.3 million prisoners, place them in job-skill programs and find them work and housing.

Police must be demilitarized. Mass surveillance must end. Undocumented workers must be given citizenship and full protection under the law. NAFTA, CAFTA and other free-trade agreements must be revoked. Anti-labor laws such as the Taft-Hartley Act, along with laws that criminalize poverty and dissent, must be repealed.Comment

-

Re: One You Get Started . . .

She makes a few good points. Ignore the host. He's lost.

Comment

-

Re: One You Get Started . . .

Originally posted by Thailandnotes View Post

I like Chris Hedges. He's a compassionate man who lives his life with integrity and I greatly respect him.

But I VEHEMENTLY disagree with much if not most of what he proposes. The highlights in green I agree or strongly agree with; those in red I absolutely oppose.Comment

-

Re: One You Get Started . . .

Originally posted by Raz View Post

Thanks Raz, for that concise review. I would argue in favor of breaking up giant corporations. When business concerns get as big as they are now, they run things, as we see in the leaked portions of the trans pacific partnership. If we keep them smaller the governments stay sovereign.Comment

of all Americans, not something accessible for the wealthy alone.

of all Americans, not something accessible for the wealthy alone.

Comment