-

-

Re: an oversupply of almost everything?

I haven't read her posts since she was writing at the Oil Drum as "Gail the Actuary". Too bad that site is gone, it was one of the best. Unfortunately her ideas were mostly less than insightful. That doesn't appear to have changed here. If workers have too little capital to create demand then investors should be less greedy and throw the "common" workers a bone so they have the money to soak up demand. It seems simple enough but she thinks the problem is that "investors can no longer find investments that provide an adequate return on capital...". No thinking person should give a F*** about investors. Those are people with way more money than ideas. It the tax system was balanced, workers would have more and investors less...problem solved.Originally posted by lektrode View Post -

Re: an oversupply of almost everything?

Very interesting ideas: trying to explain the economic implications of limited supply of raw materials.

"6. An �upside down� peak oil story.

Most people in the peak oil community believe what economists say about supply and demand�namely, that oil prices will rise if there is a supply problem. They have not realized that in a networked economy, wages and prices are tightly linked. The way limits apply is not necessarily the way we expect. Limits may come through a lack of good paying jobs, and because of this lack of jobs, inability to purchase products containing oil.

The connection between energy and jobs is clear. Good jobs require the use of energy, such as electricity and oil; lack of good-paying jobs is likely to be a manifestation of an inadequate supply of cheap energy. Also, high paying jobs are what allow rising buying power, and thus keep demand high. Thus, oil limits may appear as a demand problem, with low oil prices, rather than as a high oil price problem.

In my opinion, what we are seeing now is a manifestation of peak oil. It is just happening in an upside down way relative to what most were expecting.

* * *

Conclusion

One way of viewing our problem today is as a crisis of affordability. Young people cannot afford to start families or buy new homes because of a combination of the high cost of higher education (leading to debt), the high cost of fuel-efficient new cars (again leading to debt), the high cost of resale homes, and the relatively low wages paid to young workers. Even older workers often have an affordability problem. Many have found their wages stagnating or falling at the same time that the cost of healthcare, cars, electricity, and (until recently) oil rises. A recent Gallop Survey showed an increasing share of workers categorize themselves as �working class� rather than �middle class.�

It is this affordability crisis that is bringing the system down. Without adequate wages, the amount of debt that can be added to the system lags as well. It becomes impossible to keep prices of commodities up at a high enough level to encourage production of these commodities. Return on investment tends to be low for the same reason. Most researchers have not recognized these problems, because they are narrowly focused and assume that models that worked in the past will continue to work today."Comment

-

Re: an oversupply of almost everything?

Profitability from Debt has taken the place of profitability from Production.Comment

-

Re: an oversupply of almost everything?

never mind 'the profitability from corruption'...Originally posted by don View PostComment

-

Re: an oversupply of almost everything?

Yeah I love finance. I have mentioned it in comparison to water before. They might call the drought in California a serious problem. One might assume everyone would rejoice when it rains. However if water begins to be used to secure credit, then ending the drought would have another curious new tributary to their swollen rivers, tears of financial collapse. They say nuclear energy was a Faustian bargain, but I think credit is the hand maiden of the devil. Both of them can turn fresh water into poison.

As to too much of everything, no such thing can be said in isolation or context. A million slaves might want an ice tea at high noon picking cotton, but without leave or purchasing power , not one of them will sell. So is it an over supply or a lack of purchasing power? Finacial equalibrium can be demonstrated with either a 100 freemen, or one master and 99 slaves. Another gift of finance.Comment

-

Re: an oversupply of almost everything?

an even 'better' example of the Faustian bargain ?Originally posted by gwynedd1 View Post

the 535+1 clowns of the beltway, who's slavery to debt, beholden-to/bought-by the string-pullers who 'finance' their continuing in office year after year after yearComment

-

Re: an oversupply of almost everything?

Corruption is found in every system. Preferring debt over production is a new paradigm . . . .Originally posted by lektrode View Post

"let's do it again, nipper . . . ."

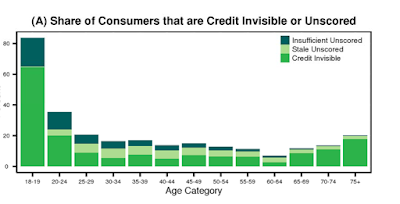

A recently released government study by the Consumer Financial Protection Bureau on "Credit Invisibles" has some interesting facts on people with and without credit histories.

- [*=left]Approximately 188.6 million Americans have credit records at one of the NCRAs that can be scored by the commercially-available model. This represents over 80 percent of the adult population.

[*=left]An additional 19.4 million Americans, representing 8.3 percent of the adult population, have credit records that cannot be scored. These are almost evenly split between consumers with credit records that are insufficient unscored (9.9 million) and those that are stale unscored (9.6 million).

[*=left]The remaining 11 percent of adults, or about 26 million Americans, are credit invisible.

[*=left]Over 80 percent of 18 or 19 year olds are credit invisible or have unscored records. This percentage drops substantially for older consumers, falling below 40 percent in total for the 20 to 24 year old age group. After age 60, the number of consumers that are credit invisible or that have an unscored record increases with age.

[*=left]Over 10 million of the estimated 26 million credit invisibles are younger than 25. Consumers in this age group also account for a disproportionate share of insufficient-unscored credit records. In contrast, most consumers with stale-unscored records are middle aged. Consumers aged between 25 and 50 account for over half of stale-unscored credit records.

Percentage Share of Invisibles and Unscored by Age

Number of Invisibles and Unscored by Age

Credit Expansion

The study did not indicate how many of the 45 million (invisibles plus unscorables) are illegal aliens. But the name of the game as always is credit expansion.

Investor's Business Daily discusses situation in Obama Pushing Banks Into Riskiest Borrower Pool Yet: 45 Million 'Unscorables'.

Housing: As part of its amnesty program, the Obama regime seeks to expand credit to a whopping 45 million potential deadbeats � including illegal immigrants � whose credit files are too spotty even to score for risk.

In a just-released federal report, the administration portrays these "credit invisibles" as victims of a traditional credit-scoring system. And since most are minorities, it claims that excluding them from the financial mainstream is discriminatory.

"Our report found that black and Hispanic consumers are more likely than white or Asian consumers to have limited credit records," CFPB Director Richard Cordray said in a press call.

To remedy the "credit inequality," credit reporting agencies are being pressed to generate scores for this high-risk group based on payments of cellphone and utility bills, as well as immigrant remittances.

But analysts say most of these "unscorables" are not creditworthy, and according to preliminary estimates, their median credit score falls well below the subprime cutoff (535 vs. 620). Public records show many are subject to third-party debt collection and tax liens.

Lenders rely on the three-digit credit score as an indicator of how likely it is a borrower will repay a debt. Stale files or thin credit history does not allow FICO and other risk modelers to accurately predict future credit performance � that is, the likelihood, relative to other borrowers, that a consumer will become 90 or more days past due on a credit obligation in the following two years.

Using "alternative" inputs in the models, such as utility payments and remittances, could water down the models and make credit scores less reliable, leading banks to make even riskier lending decisions.

Undoing the "Card Act"

Part of the alleged credit injustice dates to 2010, when many of the provisions of the Credit Card Accountability, Responsibility, and Disclosure Act (CARD Act) took effect.

CNBC discusses the Card Act in 45 Million Americans Live Without a Credit Score

After the CARD Act passed in 2009, consumers under age 21 had to prove they had a job or a co-signer to get a credit card. The goal was to keep younger consumers from taking on credit card debt they could not repay, he said, "but if you are going to restrict people from getting credit, you are also going to restrict their ability to build a credit report."

Get a Job

Is that a real hardship to require a job or other source of documented income before giving someone a credit card or mortgage?

Instead, CNBC offers this advice on rebuilding or establishing credit.

How to Rebuild Your Credit

Consumers have a number of possible ways to build or rebuild a credit history. One thing they can do is obtain a secured credit card. A credit score is not necessary, and using the card to draw on money you deposit with a bank will help you build a credit history.

If you go this route, make sure to choose a card that will report your payment history to all three credit rating agencies, Ulzheimer cautioned. Not all do, and "without reporting to all three, it's like a tree falling in the woods," he said, because your credit history will not be known.

Becoming an authorized user on someone else's card is another option for consumers. College students may do this with a parent's card, for example. They also establish some credit history when they have a student loan. Even when they are in school and payments are deferred, the loan will show up as part of their credit history, Ulzheimer said.

Another option that is less well-known is to take out a credit builder loan from a credit union. Instead of receiving the loan money upfront, a consumer makes payments into an interest-bearing account for the life of the loan. At the end of that time, the consumer receives the money with any accrued interest.

Instead of granting credit to those with no jobs, teenagers who live at home, illegal aliens, and other non-creditworthy individuals, the CNBC advice seems reasonable enough. Instead, Obama wants another credit free-for-all to expand housing and car loans.

http://globaleconomicanalysis.blogsp...t6ZzJwQ7PUV.99

�his master's voice�

Last edited by don; May 17, 2015, 04:15 PM.Comment

- [*=left]Approximately 188.6 million Americans have credit records at one of the NCRAs that can be scored by the commercially-available model. This represents over 80 percent of the adult population.

For a concise, readable summary of iTulip concepts developed over the past 16 years and a vision of a challenging next decade and how to navigate it, read Eric Janszen's book "Post Catastrophe Economy".

Join the discussion of today's events with a wide range of professionals with an interest in economics and finance. Register to join our 50,000 plus member registered community from 78 countries today.

Subscribe to iTulip Select for access to the longest running, deep, accurate, and unvarnished macro economic trends analysis and forecasting available, since 1998.

- If this is your first visit, be sure to check out the FAQ by clicking the link above. You may have to register before you can post: click the register link above to proceed. To start viewing messages, select the forum that you want to visit from the selection below.

Working...

Tweet

Tweet

Comment