Tweet

Tweet

Re: even hudson sez so?

a few more interesting tidbits...

(1st up, from the FT via the DNC/lwr manhattan's fave $pin machine):

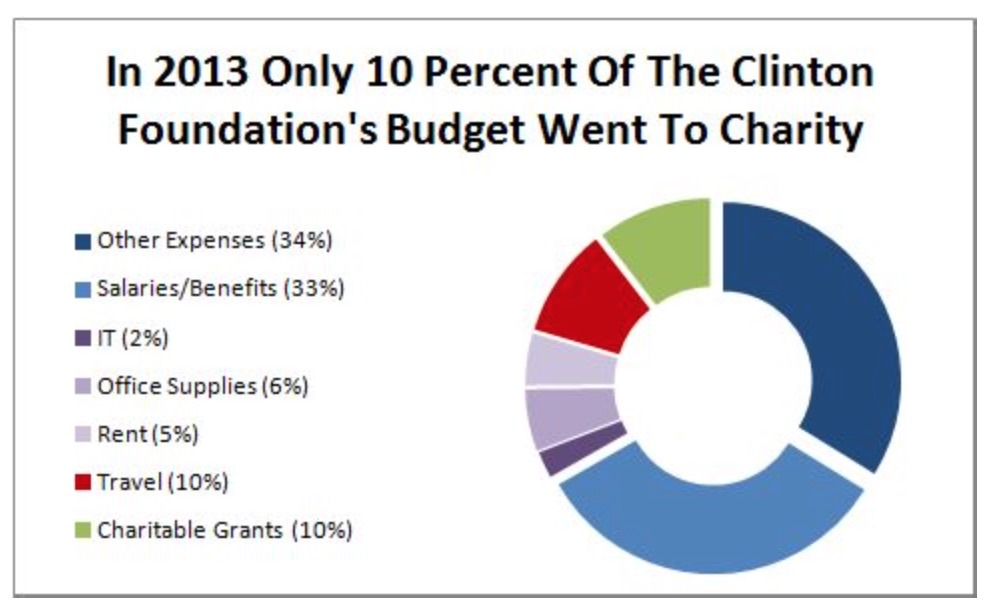

How the Clinton Scandals Can Bring Down the Democrats

lets (them) count the ways:

heheheh.... gotta lu`uv #5, esp if yer long CCJ ;)

then over at 0C, we see where the BIG money is flowing from:

Who Is Really Choosing America's Next President?

hmmm... kinda 'funny' huh - how the top 2 above add up to more - like WAAAAY more - than the rest on this list, eh?

just gotta lu`uv how its portrayed in the lamerstream media about how the kochs and the rest of 'the vast rightwing conspiracy' are

somehow tilting the field...

esp considering - from the comments at 0C - just whom the Numero Uno is?

again = probably just 'another co-incidence' ?

riiiight....

a few more interesting tidbits...

(1st up, from the FT via the DNC/lwr manhattan's fave $pin machine):

How the Clinton Scandals Can Bring Down the Democrats

lets (them) count the ways:

- Clinton Foundation: 'We Made Mistakes' The Fiscal Times

- Clinton Foundation admits missteps in donor disclosure Associated Press

- Clinton Foundation Provides Details on Canadian Donation The Wall Street Journal

- Hillary Clinton is getting bombarded with new financial scandals Business Insider

- Mitt Romney says Clinton Foundation's link to uranium deal 'looks like bribery' Business Insider

heheheh.... gotta lu`uv #5, esp if yer long CCJ ;)

then over at 0C, we see where the BIG money is flowing from:

Who Is Really Choosing America's Next President?

Submitted by Robert Faturechi and Jonathan Stray via ProPublica,

Rapid Rise in Super PACs Dominated by Single Donors

Super PACS that get nearly all of their money from one donor quadrupled their share of overall fund-raising in 2014.

Donors who launch their own PACs are seeking more control over how their money is spent. And many have complained about the commissions that fundraising consultants take off the top of their donations to outside groups. But the move carries risks if the patron is new to the arena.

Rapid Rise in Super PACs Dominated by Single Donors

Super PACS that get nearly all of their money from one donor quadrupled their share of overall fund-raising in 2014.

Donors who launch their own PACs are seeking more control over how their money is spent. And many have complained about the commissions that fundraising consultants take off the top of their donations to outside groups. But the move carries risks if the patron is new to the arena.

just gotta lu`uv how its portrayed in the lamerstream media about how the kochs and the rest of 'the vast rightwing conspiracy' are

somehow tilting the field...

esp considering - from the comments at 0C - just whom the Numero Uno is?

Steyer?

"Prior to joining Hellman & Friedman, Steyer worked at Goldman Sachs from 1983-85 as an associate in the risk arbitrage department under Robert Rubin. "

"Prior to joining Hellman & Friedman, Steyer worked at Goldman Sachs from 1983-85 as an associate in the risk arbitrage department under Robert Rubin. "

riiiight....

Comment