Tweet

Tweet

Yesterday we demonstrated that stock market valuations are not merely �on the high side� as Janet Yellen averred last week. Instead, they are positively in the nose-bleed section of history.

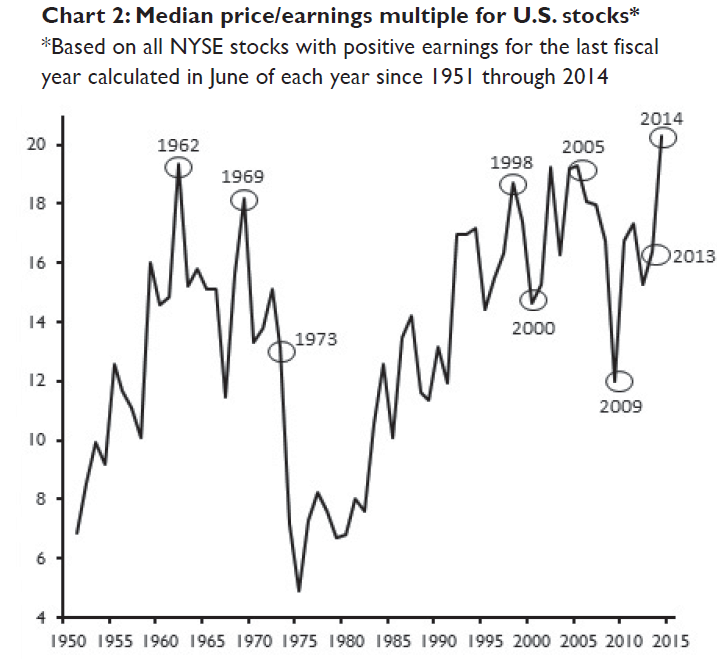

You don�t get the Russell 2000 trading at 90X honest-to-goodness GAAP earnings or 125 biotechs with aggregate LTM losses of $10 billion sporting a combined market cap of $280 billion unless you are deep into bubble land. In fact, the chart on the median PE multiple for all NYSE stocks bears repeating.

Recall this graph is based on trailing GAAP earnings for all companies with positive income. But that was for the LTM period ending in June 2014. Since then the market is up by 7%, yet reported earnings have basically flat-lined. S&P 500 earnings for the June 2014 LTM period, for example, were $103 per share��-a level that has now dropped to $102 per share for the December LTM period.

In short, the median NYSE valuation multiple is now at upwards of 22X�a level far above even the dotcom and housing bubble peaks. It is no wonder, therefore, that even a certified Cool-Aid drinker like St Louis Fed head, James Bullard, has now confessed that he fears a �violent� Wall Street sell-off when the Fed finally ends an 80 month streak of ZIRP sometime this fall.

So what are they waiting for? Actually, this morning�s

Wall Street Journal expressed it about as plaintively as it comes. In a word, the monetary politburo is waiting for zero interest rates, massive debt monetization and its wealth effects promises and �puts� to goose the macros:

The central bank has kept rates near zero since the recession to spur hiring, investment and spending.

Does it really take purportedly intelligent people six years to see that the macros are not responding? Better still, isn�t it time for the Fed to explain the exact channel by which its interest rate pegging and forward guidance is supposed to be transmitted to the main street economy?

After all, if these channels are blocked or ineffective��then its flood of liquidity never leaves the canyons of Wall Street. In that event, the central bank actually functions as a financial doomsday machine, inflating the next financial bubble until it bursts. Then, apparently, its job is to rinse and repeat.

Since housing is in the news today, its a good place to start. Historically, the concept of easing worked like a charm in this sector because the nation�s households had not yet been buried in mortgage debt, and home prices had not yet been inflated for so long that they ended up out of reach for a large portion of families.

Accordingly, when the macro-economy weakened�-usually because the Fed had previously overstimulated and had been forced to throw on the brakes�it simply pushed down the interest rate. That caused affordability and mortgage borrowing to soar, thereby kicking-in the housing investment component of a standard Fed-fueled �recovery�.

Yet that self-evidently was a one-time parlor trick, not the activation of eternal economic laws like those which govern the operations of free markets. Since this kind of easy money stimulus required a steady ratcheting up of debt relative to income, it was a mathematical necessity that sooner or later household balance sheets would be tapped out.

In fact, the Greenspan housing bubble disabled the home mortgage credit channel once and far all. On the one hand, it drove real housing prices to levels that made home purchases unaffordable for a huge portion of middle class households. Between Greenspan�s 1987 arrival at the Eccles Building, in fact, and the 2007 peak, the US housing price index soared by 160% or by nearly 3X the rise in the GDP deflator.

At the same time, it saturated the household sector with upwards of $3 trillion of MEW debt (mortgage equity withdrawal). That is, Greenspan�s policy essentially encouraged households to massively liquidate the equity in their homes to finance current non-housing purchases�� such as vacations, boats, autos and tuition��but at the expense of permanent mortgage servitude.

That is why upwards of 20 million households are either underwater on their mortgages completely or have mortgage debt so high relative to market value that the cannot generate sufficient cash to cover the down-payment and brokers fees on a �move-up� transaction.

So home finance is semi-frozen and the normal dynamic which generates turnover of the existing housing stock and demand for new construction has been badly impaired. At the same time, tepid growth of real wages and salaries have made it impossible for households to rapidly earn-out from under their existing mountain of debt.

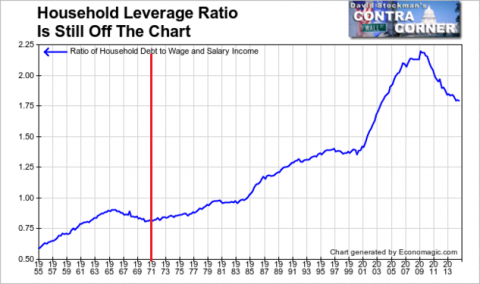

It therefore needs to be said once again: This condition of �peak debt� is a macro-economic game changer. It means that for the first time in modern history, debt ratios are being slowly reduced during a recovery, not ratcheted-up. Consequently, there is no booster shot to household spending from ZIRP. What is being spent by main street households is a function of what can be earned, not incremental debt leverage.

The data for household mortgage borrowings are dispositive. For the first time in modern history, mortgage debt outstanding has actually shrunk during the course of the recovery. And as shown in the chart below, the contrast with the Fed�s leverage ratchet mechanism in past cycles could not be more dramatic.

During the seven years after the 1981 peak, for example, household mortgage credit outstanding doubled from $1 trillion to $2 trillion in dollars of the day. Likewise, during the seven years after the 1990 peak, the Fed sharply reduced interest rates and mortgage debt soared again. This time it rose by 52%�-from $2.5 trillion to $3.7 trillion.

But it was Greenspan�s madcap rate cutting and monetary easing after the dotcom boom and bust that generated the mother of all mortgage borrowing binges. During the seven years from the Q4 2000 peak through the end of 2007, mortgage debt outstanding in the household sector exploded, rising from $4.8 trillion to $10.6 trillion.

That�s right. More mortgage debt was issued during that 84 month period than had been outstanding at the turn of the century. If the Keynesian money printers who inhabit the Eccles Building had any sense that balance sheets are important, they surely would have recognized that peak debt was nigh, and that the old standby parlor trick of cheap rates and higher leverage was over and done.

In fact, that�s exactly what happened. As of Q4 2014, outstanding household mortgage debt stood at $9.38 trillion�-down nearly 12% from its pre-crisis peak.

Its goes without saying that if your only tool is a hammer, everything looks like a nail. So in response to the financial crisis and the so-called Great Recession, the Fed not only drove money market interest rates to zero in order to stimulate household borrowing, but it effectively jumped in with both feet, purchasing upwards of $1.8 trillion of GSE mortgage debt.

In conjunction with an even greater volume of US treasury debt purchases, this unprecedented maneuver was designed to flatten out the yield curve and squeeze the traditional Treasury/GSE spread in order to drive mortgage rates to rock bottom levels. That it did�-driving mortgage rates to the sub-basement of modern history.

Even the 30-year fixed rate reached 3.3% at its low point in spring 2013, leaving the rates that had prevailed during the Greenspan boom far back in the rearview mirror. If low interest rates could trump peak debt, there would have been a mortgage borrowing boom like no other.

Except obviously there wasn�t. So what the Fed�s whole post-crisis money printing spree actually did was to cause the re-pricing of existing mortgage debt and mortgage backed securities, not the creation of new debt and new housing assets.

Needless to say, the value of mortgage debt soared in inverse proportion to the plummeting yields shown in the graph above. In the immediate sense, this was a windfall to the most affluent main street households��those with enough income adequacy and stability and enough embedded home equity to refinance their existing mortgages via the Fed�s fabulous refi machine. Yet as a policy matter, the only result was the arbitrary transfer of income from savers and depositors to about 10 million out of 115 million households which were in a position to refinance.

Even worse, it resulted in tens of billions of windfall gains to bond traders and hedge funds which were prescient enough to front-run the Feds various QE bond buying campaigns; and then to fund these dramatically appreciating �assets� on 95% repo leverage at essentially zero cost of carry. In a word, the real winners were bond speculators who earned triple digit return on the smidgeon of equity capital needed to control billions of GSE and Treasury debt.

Then again, there was no transmission of the Fed�s historic leverage magic to real rates of activity in the residential housing sector. In effect, what had been the Fed�s historic clean-up hitter in its stimulus line-up just plain struck out. As was evident last week, housing starts are still in the sub-basement.

But that is not the whole story�-and the rest of it is even worse. Our Keynesian monetary politburo is besot with the illusion that any and all �spending� is good, and that if it takes building useless pyramids or digging and filling holes to generate more GDP, so be it.

As a result, it fails to note that the production of GDP also results in the consumption of real resources, and that unless productivity, efficiency and added inputs of labor and capital are brought to the table, actual societal wealth and welfare will not be improved.

And it is here that we get to the truth about the real fiasco in the housing sector resulting from the Fed�s thirty-year drive to stimulate GDP by essentially pulling activity forward in time via higher and higher leverage. Now that we are on the other side of peak mortgage debt and real housing construction and investment has slipped to rock-bottom levels, the truth comes out. Namely, that we are effectively liquidating the housing stock��that is, reducing national wealth�� because implicit depreciation now exceeds new construction.

That is evident in the chart below. Other than during a few dark months amidst the inflation crisis of 1980-81 when mortgage rates nearly reached nearly 20%, there has never been a lower rate of real net investment in the housing stock since LBJ was finishing out his term in the White House.

That�s right. In 1968, real net investment (after depreciation) in the residential housing stock was about $180 billion (2009$). By the time Ronald Reagan left office it had reached $275 billion or 53% higher. And at the peak of the Greenspan bubble in 2005, the figure was $510 billion. By contrast, the rate of real net investment today is just $125 billion��or hardly 20% of its Fed-fueled bubble peak.

It might be argued, of course, that depreciation of the residential housing stock doesn�t matter��that the number in the NIPA accounts is just theoretical. That�s partially true, but it also ignores the bigger elephant in the room. Namely, that nearly $1.4 trillion of the GDP total that is so assiduously worshipped by our Keynesian central bankers is actually imputed housing consumption, not actual tangible spending.

And that latter number has risen by roughly 15% since the Greenspan housing construction boom peaked-out in early 2006. At the same time, new spending on residential housing construction is still 50% below the 2006 level. So for all practical purposes, the US household sector is liquidating its principal asset.

To be sure, the bean counters in the Census Bureau might well argue that NIPA accounting doesn�t matter. After all, the imputed housing services number shown in the graph below is obtained from a telephone survey in which a few thousand homeowners are asked what they would rent their house for on a monthly basis if they were in the landlord business. Surely that is one of the most arbitrary fictions in all of Federal statisticaldom��even if it does amount to nearly 9% of GDP.

But here�s the thing. You can�t rent a house that is falling apart�-even a theoretical one. So the underlying reality is this: US households are still too leveraged to invest in the residential housing stock on a net basis. The phony national GDP gains obtained by Greenspan and Bernanke during the height of their MEW bonanza will subtract from national wealth for years to come.

Meanwhile, the Fed keeps hammering on the nail of low interest rates, failing to recognize that the mortgage channel of monetary policy transmission is broken. Yet even that futile undertaking is not without its baleful consequences. To wit, while most main street households are still liquidating their overhang of mortgage debt, the very top of the income ladder has net worth and cash to spare from the bubble in financial assets, and ready access to so-called jumbo mortgages or other forms of collateralized finance against financial portfolios.

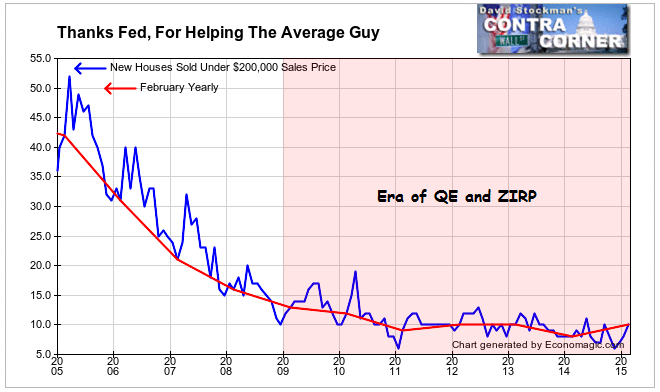

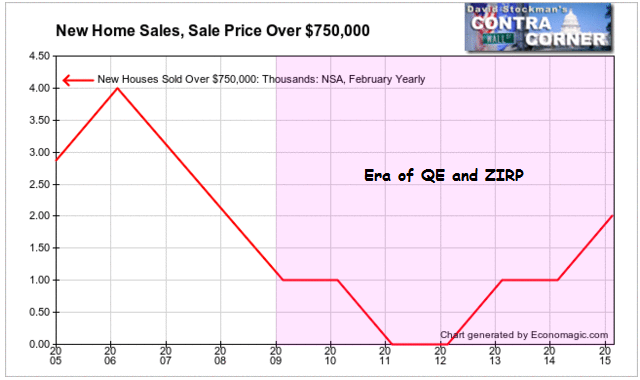

Not surprisingly, that further deformation showed up beneath the headlines in today�s new home sales release for February. As shown below, new home sales below the $200,000 median are still flat-lining on the historical bottom, while top end sales continue to rise.

New Homes Sales Over $750,000 � Click to enlarge

How in the world, it might be asked, is it possible that the chief beneficiary of the financial repression policies of the Fed is the very most affluent segment of society? That is a salient question�-but don�t bother to ask the liberal Keynesians who run the Fed. They do not even have a clue that it�s happening.

Stockman

You don�t get the Russell 2000 trading at 90X honest-to-goodness GAAP earnings or 125 biotechs with aggregate LTM losses of $10 billion sporting a combined market cap of $280 billion unless you are deep into bubble land. In fact, the chart on the median PE multiple for all NYSE stocks bears repeating.

Recall this graph is based on trailing GAAP earnings for all companies with positive income. But that was for the LTM period ending in June 2014. Since then the market is up by 7%, yet reported earnings have basically flat-lined. S&P 500 earnings for the June 2014 LTM period, for example, were $103 per share��-a level that has now dropped to $102 per share for the December LTM period.

In short, the median NYSE valuation multiple is now at upwards of 22X�a level far above even the dotcom and housing bubble peaks. It is no wonder, therefore, that even a certified Cool-Aid drinker like St Louis Fed head, James Bullard, has now confessed that he fears a �violent� Wall Street sell-off when the Fed finally ends an 80 month streak of ZIRP sometime this fall.

So what are they waiting for? Actually, this morning�s

Wall Street Journal expressed it about as plaintively as it comes. In a word, the monetary politburo is waiting for zero interest rates, massive debt monetization and its wealth effects promises and �puts� to goose the macros:

The central bank has kept rates near zero since the recession to spur hiring, investment and spending.

Does it really take purportedly intelligent people six years to see that the macros are not responding? Better still, isn�t it time for the Fed to explain the exact channel by which its interest rate pegging and forward guidance is supposed to be transmitted to the main street economy?

After all, if these channels are blocked or ineffective��then its flood of liquidity never leaves the canyons of Wall Street. In that event, the central bank actually functions as a financial doomsday machine, inflating the next financial bubble until it bursts. Then, apparently, its job is to rinse and repeat.

Since housing is in the news today, its a good place to start. Historically, the concept of easing worked like a charm in this sector because the nation�s households had not yet been buried in mortgage debt, and home prices had not yet been inflated for so long that they ended up out of reach for a large portion of families.

Accordingly, when the macro-economy weakened�-usually because the Fed had previously overstimulated and had been forced to throw on the brakes�it simply pushed down the interest rate. That caused affordability and mortgage borrowing to soar, thereby kicking-in the housing investment component of a standard Fed-fueled �recovery�.

Yet that self-evidently was a one-time parlor trick, not the activation of eternal economic laws like those which govern the operations of free markets. Since this kind of easy money stimulus required a steady ratcheting up of debt relative to income, it was a mathematical necessity that sooner or later household balance sheets would be tapped out.

In fact, the Greenspan housing bubble disabled the home mortgage credit channel once and far all. On the one hand, it drove real housing prices to levels that made home purchases unaffordable for a huge portion of middle class households. Between Greenspan�s 1987 arrival at the Eccles Building, in fact, and the 2007 peak, the US housing price index soared by 160% or by nearly 3X the rise in the GDP deflator.

At the same time, it saturated the household sector with upwards of $3 trillion of MEW debt (mortgage equity withdrawal). That is, Greenspan�s policy essentially encouraged households to massively liquidate the equity in their homes to finance current non-housing purchases�� such as vacations, boats, autos and tuition��but at the expense of permanent mortgage servitude.

That is why upwards of 20 million households are either underwater on their mortgages completely or have mortgage debt so high relative to market value that the cannot generate sufficient cash to cover the down-payment and brokers fees on a �move-up� transaction.

So home finance is semi-frozen and the normal dynamic which generates turnover of the existing housing stock and demand for new construction has been badly impaired. At the same time, tepid growth of real wages and salaries have made it impossible for households to rapidly earn-out from under their existing mountain of debt.

It therefore needs to be said once again: This condition of �peak debt� is a macro-economic game changer. It means that for the first time in modern history, debt ratios are being slowly reduced during a recovery, not ratcheted-up. Consequently, there is no booster shot to household spending from ZIRP. What is being spent by main street households is a function of what can be earned, not incremental debt leverage.

The data for household mortgage borrowings are dispositive. For the first time in modern history, mortgage debt outstanding has actually shrunk during the course of the recovery. And as shown in the chart below, the contrast with the Fed�s leverage ratchet mechanism in past cycles could not be more dramatic.

During the seven years after the 1981 peak, for example, household mortgage credit outstanding doubled from $1 trillion to $2 trillion in dollars of the day. Likewise, during the seven years after the 1990 peak, the Fed sharply reduced interest rates and mortgage debt soared again. This time it rose by 52%�-from $2.5 trillion to $3.7 trillion.

But it was Greenspan�s madcap rate cutting and monetary easing after the dotcom boom and bust that generated the mother of all mortgage borrowing binges. During the seven years from the Q4 2000 peak through the end of 2007, mortgage debt outstanding in the household sector exploded, rising from $4.8 trillion to $10.6 trillion.

That�s right. More mortgage debt was issued during that 84 month period than had been outstanding at the turn of the century. If the Keynesian money printers who inhabit the Eccles Building had any sense that balance sheets are important, they surely would have recognized that peak debt was nigh, and that the old standby parlor trick of cheap rates and higher leverage was over and done.

In fact, that�s exactly what happened. As of Q4 2014, outstanding household mortgage debt stood at $9.38 trillion�-down nearly 12% from its pre-crisis peak.

Its goes without saying that if your only tool is a hammer, everything looks like a nail. So in response to the financial crisis and the so-called Great Recession, the Fed not only drove money market interest rates to zero in order to stimulate household borrowing, but it effectively jumped in with both feet, purchasing upwards of $1.8 trillion of GSE mortgage debt.

In conjunction with an even greater volume of US treasury debt purchases, this unprecedented maneuver was designed to flatten out the yield curve and squeeze the traditional Treasury/GSE spread in order to drive mortgage rates to rock bottom levels. That it did�-driving mortgage rates to the sub-basement of modern history.

Even the 30-year fixed rate reached 3.3% at its low point in spring 2013, leaving the rates that had prevailed during the Greenspan boom far back in the rearview mirror. If low interest rates could trump peak debt, there would have been a mortgage borrowing boom like no other.

Except obviously there wasn�t. So what the Fed�s whole post-crisis money printing spree actually did was to cause the re-pricing of existing mortgage debt and mortgage backed securities, not the creation of new debt and new housing assets.

Needless to say, the value of mortgage debt soared in inverse proportion to the plummeting yields shown in the graph above. In the immediate sense, this was a windfall to the most affluent main street households��those with enough income adequacy and stability and enough embedded home equity to refinance their existing mortgages via the Fed�s fabulous refi machine. Yet as a policy matter, the only result was the arbitrary transfer of income from savers and depositors to about 10 million out of 115 million households which were in a position to refinance.

Even worse, it resulted in tens of billions of windfall gains to bond traders and hedge funds which were prescient enough to front-run the Feds various QE bond buying campaigns; and then to fund these dramatically appreciating �assets� on 95% repo leverage at essentially zero cost of carry. In a word, the real winners were bond speculators who earned triple digit return on the smidgeon of equity capital needed to control billions of GSE and Treasury debt.

Then again, there was no transmission of the Fed�s historic leverage magic to real rates of activity in the residential housing sector. In effect, what had been the Fed�s historic clean-up hitter in its stimulus line-up just plain struck out. As was evident last week, housing starts are still in the sub-basement.

But that is not the whole story�-and the rest of it is even worse. Our Keynesian monetary politburo is besot with the illusion that any and all �spending� is good, and that if it takes building useless pyramids or digging and filling holes to generate more GDP, so be it.

As a result, it fails to note that the production of GDP also results in the consumption of real resources, and that unless productivity, efficiency and added inputs of labor and capital are brought to the table, actual societal wealth and welfare will not be improved.

And it is here that we get to the truth about the real fiasco in the housing sector resulting from the Fed�s thirty-year drive to stimulate GDP by essentially pulling activity forward in time via higher and higher leverage. Now that we are on the other side of peak mortgage debt and real housing construction and investment has slipped to rock-bottom levels, the truth comes out. Namely, that we are effectively liquidating the housing stock��that is, reducing national wealth�� because implicit depreciation now exceeds new construction.

That is evident in the chart below. Other than during a few dark months amidst the inflation crisis of 1980-81 when mortgage rates nearly reached nearly 20%, there has never been a lower rate of real net investment in the housing stock since LBJ was finishing out his term in the White House.

That�s right. In 1968, real net investment (after depreciation) in the residential housing stock was about $180 billion (2009$). By the time Ronald Reagan left office it had reached $275 billion or 53% higher. And at the peak of the Greenspan bubble in 2005, the figure was $510 billion. By contrast, the rate of real net investment today is just $125 billion��or hardly 20% of its Fed-fueled bubble peak.

It might be argued, of course, that depreciation of the residential housing stock doesn�t matter��that the number in the NIPA accounts is just theoretical. That�s partially true, but it also ignores the bigger elephant in the room. Namely, that nearly $1.4 trillion of the GDP total that is so assiduously worshipped by our Keynesian central bankers is actually imputed housing consumption, not actual tangible spending.

And that latter number has risen by roughly 15% since the Greenspan housing construction boom peaked-out in early 2006. At the same time, new spending on residential housing construction is still 50% below the 2006 level. So for all practical purposes, the US household sector is liquidating its principal asset.

To be sure, the bean counters in the Census Bureau might well argue that NIPA accounting doesn�t matter. After all, the imputed housing services number shown in the graph below is obtained from a telephone survey in which a few thousand homeowners are asked what they would rent their house for on a monthly basis if they were in the landlord business. Surely that is one of the most arbitrary fictions in all of Federal statisticaldom��even if it does amount to nearly 9% of GDP.

But here�s the thing. You can�t rent a house that is falling apart�-even a theoretical one. So the underlying reality is this: US households are still too leveraged to invest in the residential housing stock on a net basis. The phony national GDP gains obtained by Greenspan and Bernanke during the height of their MEW bonanza will subtract from national wealth for years to come.

Meanwhile, the Fed keeps hammering on the nail of low interest rates, failing to recognize that the mortgage channel of monetary policy transmission is broken. Yet even that futile undertaking is not without its baleful consequences. To wit, while most main street households are still liquidating their overhang of mortgage debt, the very top of the income ladder has net worth and cash to spare from the bubble in financial assets, and ready access to so-called jumbo mortgages or other forms of collateralized finance against financial portfolios.

Not surprisingly, that further deformation showed up beneath the headlines in today�s new home sales release for February. As shown below, new home sales below the $200,000 median are still flat-lining on the historical bottom, while top end sales continue to rise.

New Homes Sales Over $750,000 � Click to enlarge

How in the world, it might be asked, is it possible that the chief beneficiary of the financial repression policies of the Fed is the very most affluent segment of society? That is a salient question�-but don�t bother to ask the liberal Keynesians who run the Fed. They do not even have a clue that it�s happening.

Stockman