Tweet

Tweet

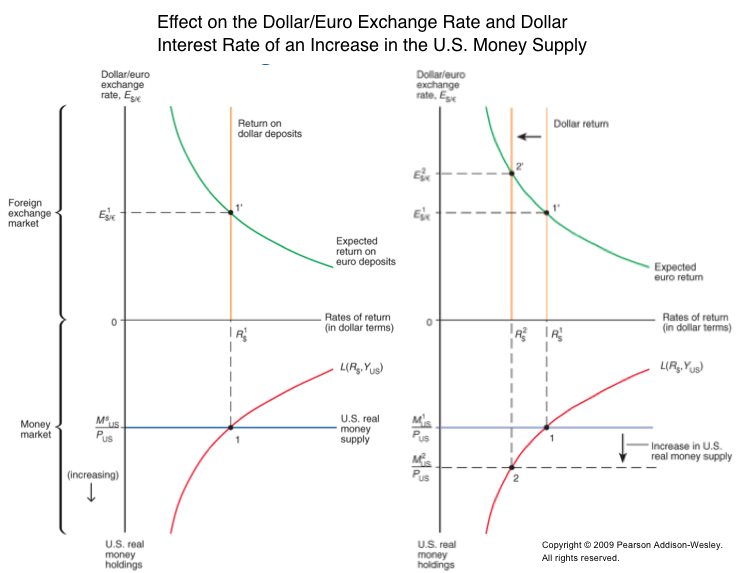

The information below is from an article by AE-P of the Daily Telegraph. In the situation described below I would like to know what people think would happen to European interest rates. If it is like Japan then one would expect them to remain low for a long time, but with the possibility of the European Union breaking up this may not happen as each country will have to raise funds in an environment of uncertainty.

Mr Legrain said the failure to stress test for deflation is a grave error. Given that it would wreak havoc with banks� balance sheets, it is a farce. Deflation raises real interest rates and it raises the debt burden,� he said.

Even �lowflation� of around 0.5pc is already causing debt ratios to shoot up across southern Europe, rising by 5pc of GDP each year in Italy despite a large primary surplus. A deflationary trap would revive fears of a debt crisis in these countries, with contagion effects for banks holding government bonds. The �vicious circle� between the states and banks remains despite talk of a banking union.

�It is very telling that the ECB chose to ignore deflation because they themselves are responsible for it,� said Professor Richard Werner, from Southampton University and a former adviser to Japan.

�What we learned in Japan is that deflation automatically leads to bankruptcies because nominal GDP is shrinking. Japan had 20 big banks in 1990 and now it has three. Deflation was the mechanism that brought this about. The ECB is following exactly in the footsteps of the Bank of Japan,� he said.

Mr Legrain said the failure to stress test for deflation is a grave error. Given that it would wreak havoc with banks� balance sheets, it is a farce. Deflation raises real interest rates and it raises the debt burden,� he said.

Even �lowflation� of around 0.5pc is already causing debt ratios to shoot up across southern Europe, rising by 5pc of GDP each year in Italy despite a large primary surplus. A deflationary trap would revive fears of a debt crisis in these countries, with contagion effects for banks holding government bonds. The �vicious circle� between the states and banks remains despite talk of a banking union.

�It is very telling that the ECB chose to ignore deflation because they themselves are responsible for it,� said Professor Richard Werner, from Southampton University and a former adviser to Japan.

�What we learned in Japan is that deflation automatically leads to bankruptcies because nominal GDP is shrinking. Japan had 20 big banks in 1990 and now it has three. Deflation was the mechanism that brought this about. The ECB is following exactly in the footsteps of the Bank of Japan,� he said.

Comment