-

-

Re: China in the Shadows

Uh oh is right.Rut Roh Rorge ...

When I saw last week that the IMF was not even going to consider voting on the RMB inclusion into the SDR basket in October I surmised that the pressure to devalue was too great on the PBoC.

That was the largest currency peg move by the PBoC ever I believe.

China still has a long way to go with rates at 4.8% to get to ZIRP but they could be there within a year if troubles continue.Comment

-

Re: China in the Shadows

What China’s Devaluation Means to the U.S. Economy

By Pam Martens and Russ Martens: August 11, 2015

Markets received a seismic jolt from China on Tuesday as it devalued its currency, the Yuan, by the most in two decades, cutting its daily reference rate by 1.9 percent. The move sparked instant selloffs in stocks, commodities, and emerging market currencies as well as a drop in the yield of the 10-year U.S. Treasury Note, which is trading early this morning at a yield of 2.16 percent.

The devaluation was interpreted in the markets as a sign of capitulation by China to forego a stable currency policy in a last-ditch effort to revitalize sluggish export growth. On Friday, China reported that its exports had plunged by 8.3 percent overall in July with dramatic declines of 12.3 percent to the European Union and 13 percent to Japan. Exports to the United States fell by 1.3 percent.

While China announced that the currency devaluation was a one-off move, the prevailing fear in global markets is that it marks a new round in the raging currency wars where countries are now competing to debase their currencies in hopes of making their exports more competitively priced in global markets.

The move spells trouble for the U.S. on a number of fronts. As of 8:39 a.m. in New York, stock futures on the Dow Jones Industrial Average were in the red by 147 points.

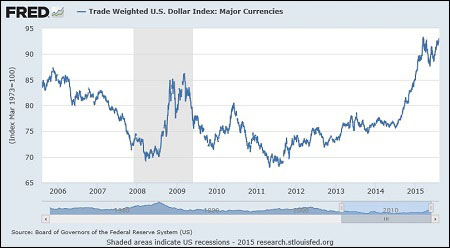

The U.S. imports more goods from China than any other country. Through June of this year, the U.S. had imported $226.7 billion in goods from China versus $150.4 billion from Canada and $145.1 billion from Mexico, according to the U.S. Census Bureau. The Federal Reserve has been struggling to avoid importing deflation into the U.S.; this devaluation move now means that Chinese goods flowing into the U.S. just got cheaper and the ability of U.S. exporters to compete in global markets just got a lot harder.

According to a Federal Reserve report released on July 17, the rising value of the U.S. Dollar is having a significant negative impact on large U.S. based multinationals. The report noted that “The dollar’s strength likely explains roughly a third of the recent decline in profits earned from foreign subsidiaries” and that “Firms with high foreign sales tend to be larger and account for almost 75 percent of S&P 500 nonfinancial earnings excluding oil and utilities.”

As we have reported before, this global currency race to the bottom cannot be solved by central banks. The problem is directly rooted in the unprecedented levels of income and wealth inequality that plague this era. In the U.S., that problem springs directly from Wall Street’s institutionalized wealth transfer system.

and from Asia Times . . .

China yuan devaluation: Let he who hasn’t sinned …

BY CHAN AKYA on in

Last edited by don; August 11, 2015, 10:21 AM.Comment

-

Re: China in the Shadows

This is fascinating to me.

Most of the theories we use to explain and understand relative currency strength are based upon the fundamental assumption of a free market filled with many rational actors.

China is a command economy controlled by a communist dictatorship and always has been.

Though China has recently behaved like a free market in some ways, they have never really been one.

In recent years the large western democracies have drifted into central control of their own financial markets with the heavy-handed action of their central banks, along with unprecedented consolidation of commercial banks and financial institutions into near monopolies.

Free markets with many rational actors are not the case here.

Our beloved theories may not work at all.Comment

-

Re: China in the Shadows

As it is visible on picture US has not big amount of ships. Modern ships but on the sea amount of ships just counts as seas are huge. Per my understanding there are 3 scenarios debated in US how to attack China with only one of them includes attacks on China main land. This one could be too ambitious,scares US allies and could be interpreted as escalation by Chinese when both 2 scenarios left is about blocking China. Some US allies like South Korea is just not possible to defend so I wonder when some of them will change thier orientation to China.Originally posted by don View PostComment

-

Re: China in the Shadows

EJ has commented that the G20 have a gentleman's agreement to take turns devaluing their currencies.

The Yaun has appreciated greatly over the last year due to it's peg to the rising US dollar.

Maybe it was just China's turn to devalue.Comment

-

Re: China in the Shadows

The principals may be in compliance, knowing the degree of global crisis we're in. Analogous to the 1930s.EJ has commented that the G20 have a gentleman's agreement to take turns devaluing their currencies.

The Yaun has appreciated greatly over the last year due to it's peg to the rising US dollar.

Maybe it was just China's turn to devalue.Comment

-

Re: China in the Shadows

The days of 13 or 14 CBGs are already well and truly over.Originally posted by Woodsman View Post

The days of carrier centric naval superiority may be going the way of the battleship anyway due to technological advancement, not just slow financial implosion.Comment

-

Re: China in the Shadows

I couldn't even imagine a scenario where US naval forces would directly attack the Chinese mainland short of total war.Originally posted by sandwind View Post

US Navy involvement in some sort of blockade a la the Cuban Missile crisis perhaps, but even that would be an incredibly serious escalation.

i don't understand the part about it not being possible for the US to defend South Korea, for two reasons:

1) the U.S. Already maintains considerable forces in South Korea as well as well coordinated plans for rapidly surging more to the Korean peninsula

2) South Korea possesses one of the most powerful and modern military forces in the world even if US forces packed up and left tomorrow. Surpringly that also includes growing South Korean expeditionary naval force.

Ive personally seen South Korean naval forces in a number of places thousands of miles from Korea.

Where Korea aligns in the future?

Who knows?

as its a strange 3 way relationship between China, Japan, and Korea. A lot of long simmering animosity below the surface.

I reckon the US plays a key role in it as a means for Korea and/or Japan to sit on the fence rather than choose a side.

Maybe a bit more like what India has done. Non aligned, semi-aligned, or aligned depending on issue.Comment

-

Re: China in the Shadows

China in my opinion is absolutely zero threat to the world in terms of boots on the ground military advancement. The Chinese brass and military if they tried that would crumble within weeks as they always have.Originally posted by lakedaemonian View Post

They allowed a far smaller Japanese force to crush them during WWII, and have historically had disastrous external military campaigns as far back as Chinese history goes, including the An Lushan rebellion.

Now technology wise, that is a different story. Hacking and control of strategic resources is where China excels. This may well be unstoppable.Comment

-

Re: China in the Shadows

Originally posted by ProdigyofZen View Post

Is this the reason why Warren Buffett invested in IBM? Maybe he sees something we that we don't?

Cloud systems are prone to being hacked. Better to put everything into mainframes.Comment

-

Re: China in the Shadows

I look at IBM and the only way I see them surviving is suckling at the government teat by becoming a big-time government contractor. In the private sector, IBM has done far too much damage to itself over the past few decades thanks to poor management and it cannot compete with better-run companies that are now behemoths flush with cash.Originally posted by touchring View Post

Personally, I think Buffett made a very bad investment buying all those shares of IBM. It's strange how he has stated in the past that he does not invest in technology companies and yet he now has a huge stake in IBM.

It'll be interesting to see what, if anything, IBM has up its sleeve that would convince Buffett to make such a large investment on what I see as a company with a very bleak future.Comment

-

Re: China in the Shadows

definitely another take on the devaluation . . . .

The People’s Bank of China is Magnificently Right

BY ASIA UNHEDGED on in

Comment

-

Re: China in the Shadows

Thanks for that Don. They have no clue what will happen if China unpegs their currency.

Anyone have that chart/post that EJ posted over a year ago about the external debt of China and how they were setting up for a sudden stop?Comment

-

Re: China in the Shadows

Is this the one you were thinking of, PoZ? From this thread?Originally posted by ProdigyofZen View Post

http://www.itulip.com/forums/showthr...-Janszen/page2

Comment

For a concise, readable summary of iTulip concepts developed over the past 16 years and a vision of a challenging next decade and how to navigate it, read Eric Janszen's book "Post Catastrophe Economy".

Join the discussion of today's events with a wide range of professionals with an interest in economics and finance. Register to join our 50,000 plus member registered community from 78 countries today.

Subscribe to iTulip Select for access to the longest running, deep, accurate, and unvarnished macro economic trends analysis and forecasting available, since 1998.

- If this is your first visit, be sure to check out the FAQ by clicking the link above. You may have to register before you can post: click the register link above to proceed. To start viewing messages, select the forum that you want to visit from the selection below.

Tweet

Tweet

Comment