Tweet

Tweet

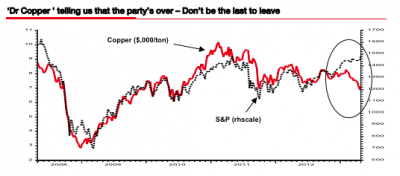

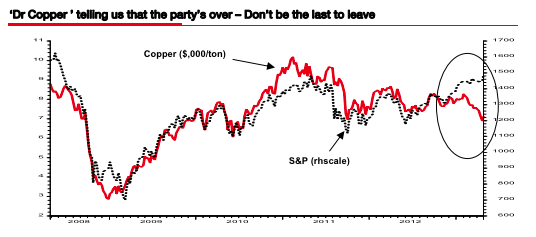

With the S&P 500 making a fresh run higher at pixel time, it would be rude not to share the latest thoughts of Albert Edwards, Socgen�s Ice Age bear. Rather than gawping stocks, he reckons we should be mindful of the red metal�

Edwards� central argument is that just as both the US and Europe are slipping towards outright deflation, investors have convinced themselves they just have to participate in the liquidity fueled frenzy offered by unlimited QE.

But the copper price is saying something different � and it offers a solid reminder that liquidity itself can disappear very quickly indeed, as it did when Edwards� last drew our attention to �Dr Copper� (and Wile E. Coyote) back in January, 2007�

Edwards� central argument is that just as both the US and Europe are slipping towards outright deflation, investors have convinced themselves they just have to participate in the liquidity fueled frenzy offered by unlimited QE.

But the copper price is saying something different � and it offers a solid reminder that liquidity itself can disappear very quickly indeed, as it did when Edwards� last drew our attention to �Dr Copper� (and Wile E. Coyote) back in January, 2007�

Too often we hear the spurious argument that liquidity is a key reason for buoyant markets, but ample liquidity is caused by good price momentum rather than the other way around. Liquidity is the caravan not the car, and if they both go too fast it will all become horribly unstable�

We think many commentators often have their causality the wrong way round. It is price momentum that causes people to borrow and speculate on further price movement. Liquidity can accentuate a market movement that is already underway. But as copper investors will testify, if the fundamentals are sufficiently undermining, liquidity arguments are not worth the paper they are written on. Poof! Liquidity can evaporate overnight.

In the event, Edwards was four or five months early. This is what he�s saying now�We think many commentators often have their causality the wrong way round. It is price momentum that causes people to borrow and speculate on further price movement. Liquidity can accentuate a market movement that is already underway. But as copper investors will testify, if the fundamentals are sufficiently undermining, liquidity arguments are not worth the paper they are written on. Poof! Liquidity can evaporate overnight.

Back in 2007 investors were convinced that markets would remain buoyant because there was ample liquidity. In a note back then we said that this was a false crutch for investors and that the liquidity would vanish from the markets if price momentum took a turn for the worse (see The Economist � link). I have exactly the same view now. In the same way that QE seems, in large part, to be bypassing the real economy, liquidity will evaporate from equities if we dive into a deflationary recession. Where will all the liquidity then go as QE is ramped up still further? It will go into ridiculously expensive bonds. Copper is acting exactly as it did when I wrote about the impotence of liquidity in the face of the (then imminent) 2007 recession. Once again it is giving us an early warning that liquidity will not save risk assets: time to get out of equities.

There are those who will accuse Edwards of stopped-clock-ism here. That doesn�t mean he�s not about to be right (again).http://ftalphaville.ft.com/2013/05/0...e-partys-over/

Comment