Tweet

Tweet

The US housing market is massive. You would expect this from a nation of 315,000,000+ people spanning over 50 states. So it is important to understand the various dynamics occurring over many states. In regards to single family home buyers, in most of the United States home prices are very reasonable. This is hard for some in the coastal regions to digest or even comprehend. When you look at certain markets in high priced areas, many people have a hard time penciling out the financial details. Yet with such a large number of investors purchasing with cash, a new market has been created. But if we are to take the US market and make a wide-eyed observation, we will find some good, bad, and ugly aspects of the current housing market. Whereas in 2008 through 2010, the market was dominated by the bad, ugly, and grotesque. What can we say about the current US housing market?

The Good

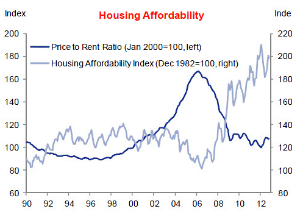

One good aspect of the market is overall, affordability is back in line to historical trends:

Price-to-rent ratios are back in line in many parts of the country. In fact, this is the big push from the all cash buyers in places like Arizona, Nevada, and Florida. The one thing I would be cautious about is in places like Arizona, you have over 50 percent of buyers coming from the investment bunch and when you look at rental prices, they are weak and vacancies are very common. But with such a high number of investors buying, you basically have investors selling to other investors thinking they will produce higher yields. However, for non-investors in most US markets prices are now affordable thanks to the big drop in prices but also the Fed�s tantalizingly low interest rates. Sure, the Fed�s balance sheet is well over $3 trillion but that is an issue for another day.

If you follow the mainstream press and use this as a barometer of what most Americans see as their primary source of information, then the Federal Reserve might as well be nuclear physics because it is never discussed or even explained. So most people are driven by the monthly nut psychology. Low rates have boosted affordability dramatically. Americans are horrible savers. Something like 50 percent of Americans do not have a retirement account.

I was having a conversation with someone and their mentality is similar to many coastal folks. �Good luck finding a property in the US for less than $300,000 in a safe area!� Of course, it is hard for some to understand that in many states, homes can be had for $100,000 in good areas and a $200,000 home will buy you a very nice spot. Heck, even in the Inland Empire in California you can find a great place for $300,000. Of course this person is obsessed with buying in prime Pasadena so good luck on that one when you have limited inventory and many other clones with similar thinking.

The Bad

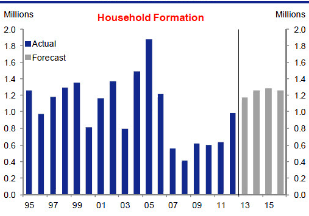

While not as good as it should be, household formation is now picking back up:

Funny how in 2005 when all you needed was a pulse for credit, household formation was up to a blistering 1.8 million per year. The crash brought on the �move in with mom, dad, or friends� trend and you can see this in 2008 where household formation was at a stunningly low 400,000. This is also another reason why the housing market is now picking up nationwide. From 2011 to 2012 household formation went from around 600,000 to a healthier 1,000,000. That is a big jump.

The one element I see getting in the way of this is the massive student debt in the market now above $1 trillion. Many younger Americans are still financially strapped so it is hard to see this improving anytime soon. Although we are nowhere close to the boom days, household formation does seem to be on an upward trend and this is a positive for housing in general.

The Ugly

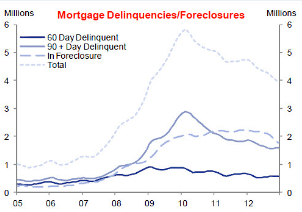

The housing market is still a mess when it comes to distressed properties:

Over 5,000,000+ Americans are in one of the following:

1,927,000 properties that are 30 or more days, and less than 90 days past due, but not in foreclosure.

1,483,000 properties that are 90 or more days delinquent, but not in foreclosure.

1,694,000 loans in foreclosure process.

The market is full of bad loans but the number is going down. Many investors buying in bulk have connections that allow them to purchase many of these properties at auction before they even hit the MLS for the regular Joe and Jane. So the low inventory is simply a manifestation of banks leaking out properties at their own pace and to select individuals.

In most parts of the US, the housing market is fairly normal based on price and financing options. However, in places like California good luck buying a home when many in the industry think prices will keep going up and bidding wars are now fairly common. Get your PowerPoint presentation ready and your heart wrenching story (and wallet out) to make a bid in many prime markets. California is a boom and bust market and we�re currently in the boom phase. It is interesting how many e-mails I get where the person is actually sad and emotionally troubled that they got out bid on an $800,000 or even $1,000,000 home. Obviously you can only get so much from an e-mail but some people seem miserable because they can�t spend $1 million on a home! I got an e-mail like this from someone in San Francisco. You know what my recommendation was? Go ahead and buy because you seem absolutely miserable!

For most Americans, the decision to buy is fairly simple in today�s market. In other markets, there are definite manic like behaviors. We�re seeing some mania in California. Buying a home is a big decision yet some are willing to drop $700,000 (i.e., finance 80+ percent of the purchase) and treat this as if they were buying a car. Buying a home is a 30 year commitment for most. Many sell within 7 to 10 years but that is assuming prices keep going up. Some that bought in 2005 are still underwater today (8 years later). You want to know what was going on 30 years ago? Ronald Reagan was President, we were in the Cold War, The Red Hot Chili Peppers launched their first self-titled album, and a fixed rate mortgage was 13.4 percent.

There are good, bad, and ugly things in today�s housing market. The scope of each of these really depends on where you live in the US.

http://www.doctorhousingbubble.com/g...te-indicators/

The Good

One good aspect of the market is overall, affordability is back in line to historical trends:

Price-to-rent ratios are back in line in many parts of the country. In fact, this is the big push from the all cash buyers in places like Arizona, Nevada, and Florida. The one thing I would be cautious about is in places like Arizona, you have over 50 percent of buyers coming from the investment bunch and when you look at rental prices, they are weak and vacancies are very common. But with such a high number of investors buying, you basically have investors selling to other investors thinking they will produce higher yields. However, for non-investors in most US markets prices are now affordable thanks to the big drop in prices but also the Fed�s tantalizingly low interest rates. Sure, the Fed�s balance sheet is well over $3 trillion but that is an issue for another day.

If you follow the mainstream press and use this as a barometer of what most Americans see as their primary source of information, then the Federal Reserve might as well be nuclear physics because it is never discussed or even explained. So most people are driven by the monthly nut psychology. Low rates have boosted affordability dramatically. Americans are horrible savers. Something like 50 percent of Americans do not have a retirement account.

I was having a conversation with someone and their mentality is similar to many coastal folks. �Good luck finding a property in the US for less than $300,000 in a safe area!� Of course, it is hard for some to understand that in many states, homes can be had for $100,000 in good areas and a $200,000 home will buy you a very nice spot. Heck, even in the Inland Empire in California you can find a great place for $300,000. Of course this person is obsessed with buying in prime Pasadena so good luck on that one when you have limited inventory and many other clones with similar thinking.

The Bad

While not as good as it should be, household formation is now picking back up:

Funny how in 2005 when all you needed was a pulse for credit, household formation was up to a blistering 1.8 million per year. The crash brought on the �move in with mom, dad, or friends� trend and you can see this in 2008 where household formation was at a stunningly low 400,000. This is also another reason why the housing market is now picking up nationwide. From 2011 to 2012 household formation went from around 600,000 to a healthier 1,000,000. That is a big jump.

The one element I see getting in the way of this is the massive student debt in the market now above $1 trillion. Many younger Americans are still financially strapped so it is hard to see this improving anytime soon. Although we are nowhere close to the boom days, household formation does seem to be on an upward trend and this is a positive for housing in general.

The Ugly

The housing market is still a mess when it comes to distressed properties:

Over 5,000,000+ Americans are in one of the following:

1,927,000 properties that are 30 or more days, and less than 90 days past due, but not in foreclosure.

1,483,000 properties that are 90 or more days delinquent, but not in foreclosure.

1,694,000 loans in foreclosure process.

The market is full of bad loans but the number is going down. Many investors buying in bulk have connections that allow them to purchase many of these properties at auction before they even hit the MLS for the regular Joe and Jane. So the low inventory is simply a manifestation of banks leaking out properties at their own pace and to select individuals.

In most parts of the US, the housing market is fairly normal based on price and financing options. However, in places like California good luck buying a home when many in the industry think prices will keep going up and bidding wars are now fairly common. Get your PowerPoint presentation ready and your heart wrenching story (and wallet out) to make a bid in many prime markets. California is a boom and bust market and we�re currently in the boom phase. It is interesting how many e-mails I get where the person is actually sad and emotionally troubled that they got out bid on an $800,000 or even $1,000,000 home. Obviously you can only get so much from an e-mail but some people seem miserable because they can�t spend $1 million on a home! I got an e-mail like this from someone in San Francisco. You know what my recommendation was? Go ahead and buy because you seem absolutely miserable!

For most Americans, the decision to buy is fairly simple in today�s market. In other markets, there are definite manic like behaviors. We�re seeing some mania in California. Buying a home is a big decision yet some are willing to drop $700,000 (i.e., finance 80+ percent of the purchase) and treat this as if they were buying a car. Buying a home is a 30 year commitment for most. Many sell within 7 to 10 years but that is assuming prices keep going up. Some that bought in 2005 are still underwater today (8 years later). You want to know what was going on 30 years ago? Ronald Reagan was President, we were in the Cold War, The Red Hot Chili Peppers launched their first self-titled album, and a fixed rate mortgage was 13.4 percent.

There are good, bad, and ugly things in today�s housing market. The scope of each of these really depends on where you live in the US.

http://www.doctorhousingbubble.com/g...te-indicators/

Comment