Tweet

Tweet

ROSENBERG: For The First Time In A Long Time, I'm Talking About InflationMamta Badkar | 51 minutes ago | 752 |

Screenshot via YouTube

A few months ago, Gluskin Sheff's David Rosenberg wrote that we are in "the throes of a secular era of disinflation." Rosenberg has been a long-term Treasury bull because he's convinced inflation and interest rates will be low for a long time.

But in a surprising twist, Rosenberg talks about inflation in his new note.

He writes that 1) if the Fed is operating under "a false presumption" that output gap is at six percent, and 2) if the pace of job growth for the past three months becomes the new normal (i.e. an unemployment rate of 6.5 percent in 2014), then the Fed would end its QE program.

But if the output gap is actually lower, which is quite possible, then the Fed is burdening its balance sheet, "providing too much juice to the system", and risks inflation down the line.

"To be talking about inflation today sounds ridiculous and until recently, I agreed with that. Maybe it's partly because having been in this business for three decades and seeing the Fed make policy mistake after policy mistake – tightening too far in the rate-hike cycles and invariably overstaying its welcome during the easing phases. Today we have a +1.6% YoY real GDP growth rate, and a real Fed funds rate of -2%, which is actually closer to -4% given what the Fed is doing to its balance sheet. So this wedge between real growth and real rates is the liquidity excess that is filtering through into the financial markets, triggering excesses in come cases (like in the credit markets).

"If the output gap is actually closer to 2% or 3%, which is quite conceivable, actually, then we are talking about an equilibrium Taylor-based funds rate of 0% – not the de facto -2% that the Fed is targeting via its unconventional easing experiment – and as such, maybe adding more securities to its balance sheet is providing too much juice to the system and risks building an inflationary process in the future. And as I have said in the recent past prolonged periods of negative zero real rates never end well. The Fed historically overstays it on the easing cycle, and it is likely no different this time around."

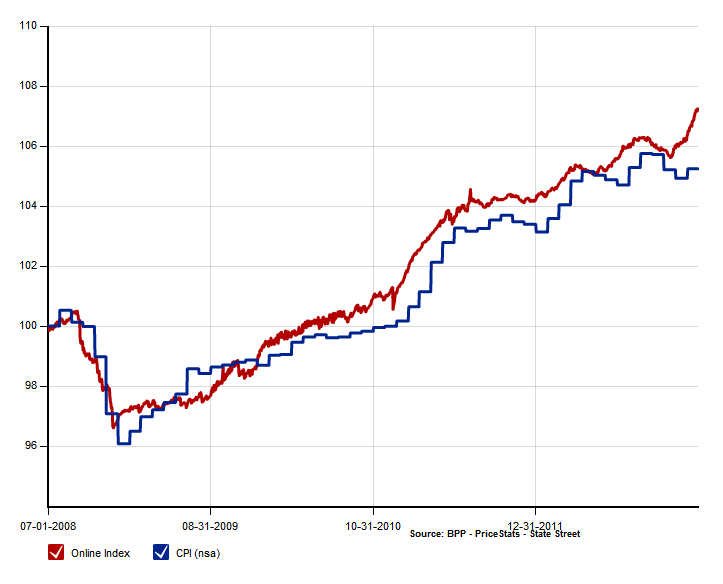

Rosenberg goes on to say that because the Fed said it would focus on both an inflation target of 2.5 percent and unemployment of 6.5 percent. In other words, he is concerned not about demand inflation, but a milder version of the "1960/1970s style of cost-push inflation." This type of inflation is driven by rising costs of labor and raw materials and is driven by supply shortage.

And in this environment he thinks those looking for yield will have to stay invested in bonds for longer.

"The reality is that the Treasury market itself does not compensate you for inflation at any part of the maturity structure out to the 10-year part of the curve. To generate a positive real yield, you have to be willing to take on a lot of duration. This is the environment the Fed has created.

"...I am not totally changing my view and I am probably way too early as I am talking for the first time in a long time about inflation. I am only detecting some tectonic shifts. Productivity waning. Wages on the rise. This means rising unit labor costs which in turn have their own correlation with inflation – like an 87% correlation (and 84% with the core CPI rate). As a long-term bond and income bull, I am not about to throw in the towel. But to reiterate I am no longer, in this profession of identifying probabilities, in the same comfort zone as I once was."

Rosenberg's note follows on David Stockman's column in the New York Times that accuses the Fed of creating a 'Great Deformation.'

- in[COLOR=#333333 !important]Share

- [COLOR=#04558B !important]2[/COLOR]

- More

Screenshot via YouTube

A few months ago, Gluskin Sheff's David Rosenberg wrote that we are in "the throes of a secular era of disinflation." Rosenberg has been a long-term Treasury bull because he's convinced inflation and interest rates will be low for a long time.

But in a surprising twist, Rosenberg talks about inflation in his new note.

He writes that 1) if the Fed is operating under "a false presumption" that output gap is at six percent, and 2) if the pace of job growth for the past three months becomes the new normal (i.e. an unemployment rate of 6.5 percent in 2014), then the Fed would end its QE program.

But if the output gap is actually lower, which is quite possible, then the Fed is burdening its balance sheet, "providing too much juice to the system", and risks inflation down the line.

"To be talking about inflation today sounds ridiculous and until recently, I agreed with that. Maybe it's partly because having been in this business for three decades and seeing the Fed make policy mistake after policy mistake – tightening too far in the rate-hike cycles and invariably overstaying its welcome during the easing phases. Today we have a +1.6% YoY real GDP growth rate, and a real Fed funds rate of -2%, which is actually closer to -4% given what the Fed is doing to its balance sheet. So this wedge between real growth and real rates is the liquidity excess that is filtering through into the financial markets, triggering excesses in come cases (like in the credit markets).

"If the output gap is actually closer to 2% or 3%, which is quite conceivable, actually, then we are talking about an equilibrium Taylor-based funds rate of 0% – not the de facto -2% that the Fed is targeting via its unconventional easing experiment – and as such, maybe adding more securities to its balance sheet is providing too much juice to the system and risks building an inflationary process in the future. And as I have said in the recent past prolonged periods of negative zero real rates never end well. The Fed historically overstays it on the easing cycle, and it is likely no different this time around."

Rosenberg goes on to say that because the Fed said it would focus on both an inflation target of 2.5 percent and unemployment of 6.5 percent. In other words, he is concerned not about demand inflation, but a milder version of the "1960/1970s style of cost-push inflation." This type of inflation is driven by rising costs of labor and raw materials and is driven by supply shortage.

And in this environment he thinks those looking for yield will have to stay invested in bonds for longer.

"The reality is that the Treasury market itself does not compensate you for inflation at any part of the maturity structure out to the 10-year part of the curve. To generate a positive real yield, you have to be willing to take on a lot of duration. This is the environment the Fed has created.

"...I am not totally changing my view and I am probably way too early as I am talking for the first time in a long time about inflation. I am only detecting some tectonic shifts. Productivity waning. Wages on the rise. This means rising unit labor costs which in turn have their own correlation with inflation – like an 87% correlation (and 84% with the core CPI rate). As a long-term bond and income bull, I am not about to throw in the towel. But to reiterate I am no longer, in this profession of identifying probabilities, in the same comfort zone as I once was."

Rosenberg's note follows on David Stockman's column in the New York Times that accuses the Fed of creating a 'Great Deformation.'

[/COLOR]

Read more: http://www.businessinsider.com/rosen...#ixzz2PKssKr00

Another one bites the dust.

He seems to be postulating some combination of hysteresis (i.e. unemployed people losing their skills and/or not innovating work processes) and cost-push inflation being generated by the actions of the Fed, both of which lead to a narrowing of the output gap, which he says is likely at 2-3% despite the sluggish GDP growth. After all, the output gap can close in two ways: actual output can rise, but potential output can also level off or fall over time. Even the CBO acknowledges that some leveling off of potential output has been taking place.

Comment