Tweet

Tweet

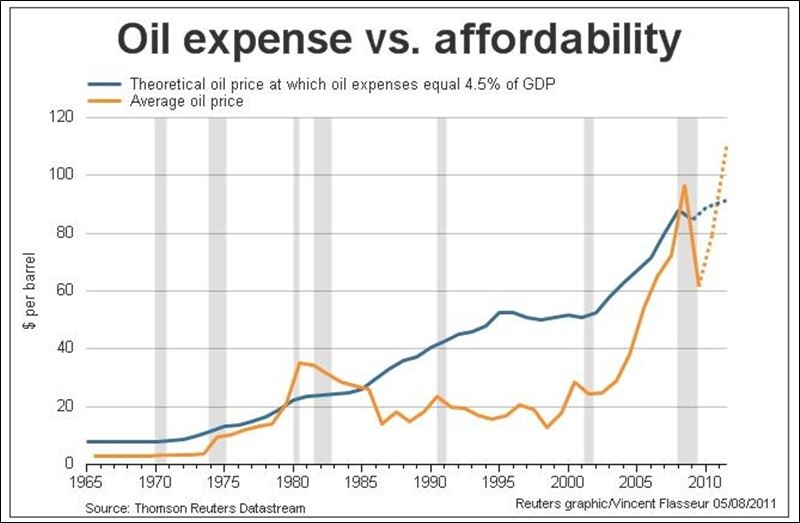

I don't think I've ever heard anyone make this argument but it's a pretty straightforward and powerful one. When you're trying to figure out whether oil prices will be a drag on economic growth, the price on it's own doesn't tell you anything relevant. Inflation adjustments give you a slightly more useful picture, but again, these are only relevant in an analysis of how many consumer goods each barrel of oil represents, something without an immediate bearing on economic growth. The ratio between prices and incomes on the other hand seems to be what really tells you what is going on: if it takes you a larger share of your income to get your oil needs met, that is a very real and quantifiable drag on what you can do.

Now here's the kicker: affordability, even at today's elevated prices, is, historically speaking, still at a very high level. Nominal GDP grows at a skyrocketing average rate of around 5% a year. I'm pretty sure the price of oil through most of history didn't rise at anywhere near a comparable speed. I don't know the exact figures, but this means that affordability should be many multiples of what it was in, say, the 1960s. If maintaining real GDP growth rates of 3% to 4% was perfectly possible in the 60s, why shouldn't it be now? It looks like the point at which oil by itself causes a breakdown of growth is very, very far off on that basis alone.

I'm not really sure how to find the relevant exact data on this, can anyone help?

caveat: the ratio of consumption ON oil inputs also fluctuates, but my guess is this effect is still dwarfed by GDP growth.

Now here's the kicker: affordability, even at today's elevated prices, is, historically speaking, still at a very high level. Nominal GDP grows at a skyrocketing average rate of around 5% a year. I'm pretty sure the price of oil through most of history didn't rise at anywhere near a comparable speed. I don't know the exact figures, but this means that affordability should be many multiples of what it was in, say, the 1960s. If maintaining real GDP growth rates of 3% to 4% was perfectly possible in the 60s, why shouldn't it be now? It looks like the point at which oil by itself causes a breakdown of growth is very, very far off on that basis alone.

I'm not really sure how to find the relevant exact data on this, can anyone help?

caveat: the ratio of consumption ON oil inputs also fluctuates, but my guess is this effect is still dwarfed by GDP growth.

Close

Close

Close

Close

Comment