Tweet

Tweet

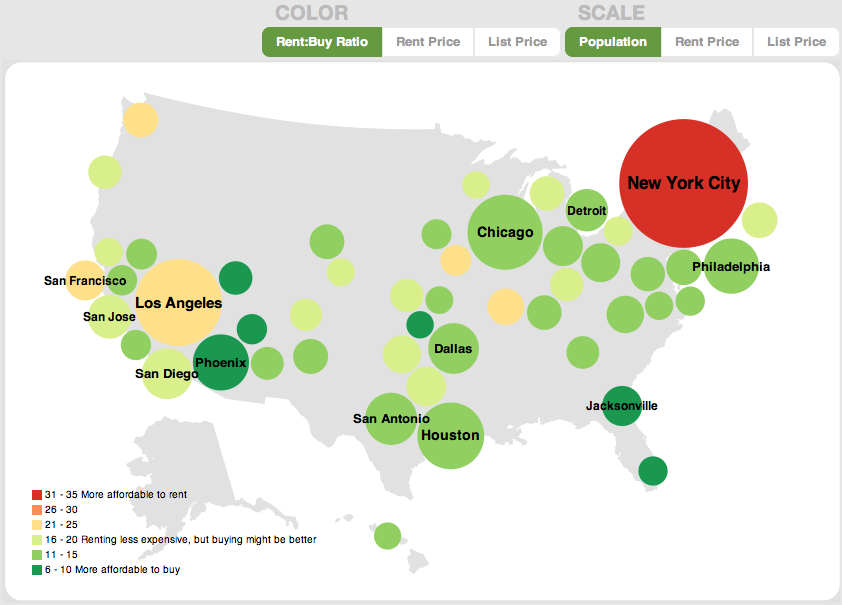

Condos in an area my wife and I have decided to live in have reached the low 100K mark, down from highs near 400K. Over the next few years they may very well drop farther. That's not in dispute. On the other hand, they don't have much further to go, unless they're thrown in for free with a car purchase

Assuming we are going to buy, should we pay cash.

The incentives:

Currently and in the near future we are getting ZIRP on the $$$.

No load origination gouging by a bank. A friend just bought a condo for 150K, putting down half. Total costs for the bank's half was 10%.

Even with historically low interest, it's nearly all interest to the bank for the first decade.

Cash buyers are getting on average a 5-10% further discount on pricing.

With our dwelling overhead reduced to a minimum, we can at least initially save, putting the $$ into PM or a cash return that's the safest/best out there short term.

All of the above dovetails with my wife's retiring from her 32 year job. Revenue streams are tightening and options more so. There is a known factor here that's appealing. Of course the neighborhood could still go to hell in 5-10 years and were stuck. I do expect the coming robust inflation to catch housing eventually, maybe 10 years from now, giving us back some pallid bonars for our trouble. Nevertheless, we haven't paid the bank a dime. I like that part . . . a lot

What do my fellow itulipers think of my situation above ? I know its not for everyone. In the past, when conditions were different and I was younger, I would never consider cash.

Assuming we are going to buy, should we pay cash.

The incentives:

Currently and in the near future we are getting ZIRP on the $$$.

No load origination gouging by a bank. A friend just bought a condo for 150K, putting down half. Total costs for the bank's half was 10%.

Even with historically low interest, it's nearly all interest to the bank for the first decade.

Cash buyers are getting on average a 5-10% further discount on pricing.

With our dwelling overhead reduced to a minimum, we can at least initially save, putting the $$ into PM or a cash return that's the safest/best out there short term.

All of the above dovetails with my wife's retiring from her 32 year job. Revenue streams are tightening and options more so. There is a known factor here that's appealing. Of course the neighborhood could still go to hell in 5-10 years and were stuck. I do expect the coming robust inflation to catch housing eventually, maybe 10 years from now, giving us back some pallid bonars for our trouble. Nevertheless, we haven't paid the bank a dime. I like that part . . . a lot

What do my fellow itulipers think of my situation above ? I know its not for everyone. In the past, when conditions were different and I was younger, I would never consider cash.

ffice" />

ffice" />

Comment