Tweet

Tweet

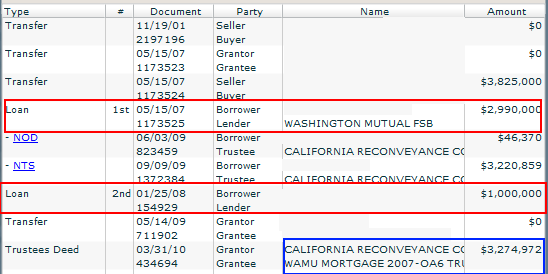

Re: When the Good Default

The modern school of economics is best known by its most visible practitioner, Alan Greenspan:

Irrational Exuberance:

Alt-A mortgages:

http://www.federalreserve.gov/boardd...23/default.htm

Subprime lending:

http://www.financialsensearchive.com...2007/1005.html

Mortgage securitization:

(same link as above)

It goes on and on and on and on and on...

Today the modern school of economics is exemplified by Ben Bernanke:

Subprime problems contained:

http://archive.newsmax.com/archives/...8/110709.shtml

No Recession in 2008:

http://money.cnn.com/2008/02/14/news...lson/index.htm

Fannie and Freddie don't face failure (!)

http://www.msnbc.msn.com/id/25704447/

And Zimbabwe Ben keeps going - like the Energizer bunny

Originally posted by WildSpitzE

Irrational Exuberance:

Clearly, sustained low inflation implies less uncertainty about the future, and lower risk premiums imply higher prices of stocks and other earning assets. We can see that in the inverse relationship exhibited by price/earnings ratios and the rate of inflation in the past. But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade?

http://www.federalreserve.gov/boardd...23/default.htm

American consumers might benefit if lenders provided greater mortgage product alternatives to the traditional fixed-rate mortgage. [Ask and ye shall receive]

http://www.financialsensearchive.com...2007/1005.html

We weren't aware of what was happening in subprime lending until late 2005 or early 2006. When we did see it - very late in the game - we were surprised at some of the things that we saw.

(same link as above)

When mortgage securitization was transferred to Wall Street, regulation became unnecessary. Investment firms, hedge funds, ratings agencies, and their ilk - these are all "self-regulating" entities. That's what you see today - these firms are all re-assessing risk and a new set of business practices is evolving.

Today the modern school of economics is exemplified by Ben Bernanke:

Subprime problems contained:

http://archive.newsmax.com/archives/...8/110709.shtml

At this juncture . . . the impact on the broader economy and financial markets of the problems in the subprime markets seems likely to be contained

http://money.cnn.com/2008/02/14/news...lson/index.htm

Federal Reserve Chairman Ben Bernanke and Treasury Secretary Henry Paulson both acknowledged problems in the U.S. economy Thursday, but both said they believe the nation will avoid falling into recession.

The two made their comments at a hearing before the Senate Banking Committee about the economy. Their testimony comes in the wake of troubling economic readings that have raised recession fears on Wall Street.

But while Paulson and Bernanke repeatedly insisted they expect the economy to avoid shifting into reverse - thanks in part to a series of interest rate cuts by the Fed and a $170 billion economic stimulus package signed by President Bush Wednesday - they conceded the economy faces additional headwinds.

Bernanke and Paulson both said the outlook for the economy is noticeably worse than it was as recently as a few months ago, and both expect cuts in official growth forecasts from the administration and the Fed in upcoming months.

The two made their comments at a hearing before the Senate Banking Committee about the economy. Their testimony comes in the wake of troubling economic readings that have raised recession fears on Wall Street.

But while Paulson and Bernanke repeatedly insisted they expect the economy to avoid shifting into reverse - thanks in part to a series of interest rate cuts by the Fed and a $170 billion economic stimulus package signed by President Bush Wednesday - they conceded the economy faces additional headwinds.

Bernanke and Paulson both said the outlook for the economy is noticeably worse than it was as recently as a few months ago, and both expect cuts in official growth forecasts from the administration and the Fed in upcoming months.

http://www.msnbc.msn.com/id/25704447/

Federal Reserve Chairman Ben Bernanke told Congress Wednesday that troubled mortgage giants Fannie Mae and Freddie Mac are in “no danger of failing.”

...

The two mortgage giants are “adequately capitalized,” Bernanke said. However, “weakness of market confidence is having an effect” on the companies, making it difficult for them to raise capital.

...

The two mortgage giants are “adequately capitalized,” Bernanke said. However, “weakness of market confidence is having an effect” on the companies, making it difficult for them to raise capital.

Comment