Tweet

Tweet

file under fiscal catastrophes....

November 13, 2009

Housing Agency�s Cash Reserves Down Sharply

By DAVID STREITFELD

The Federal Housing Administration, the government agency whose loan-insurance programs have become a crucial source of support for the housing market, said on Thursday that its cash reserves had dwindled significantly in the last year as more borrowers defaulted on their mortgages.

The agency released an audit that spelled out the rapid deterioration of its finances. It is tightening loan standards in hopes it will not become another drain on the United States Treasury, but is reluctant to clamp down so much that it snuffs out the tentative recovery in housing.

How successfully the agency walks this tightrope could well determine whether the recovery gathers force, or whether home prices slide again � perhaps creating a fresh economic downturn.

As recently as a few weeks ago, the F.H.A. had said that even under the bleakest economic forecast, its cash cushion would quickly recover. On Thursday, it abandoned that position.

�There is a real risk. Nobody has a crystal ball,� Shaun Donovan, secretary of housing and urban development, said in an interview. �We recognize there is a possibility that the reserves go below zero and stay there.�

Still, Mr. Donovan stressed that the agency, which had a role in one out of five home purchases in the last year, would not need a direct taxpayer bailout.

and why is that?

http://www.nytimes.com/2009/11/13/bu...ef=todayspaper

November 13, 2009

The agency released an audit that spelled out the rapid deterioration of its finances. It is tightening loan standards in hopes it will not become another drain on the United States Treasury, but is reluctant to clamp down so much that it snuffs out the tentative recovery in housing.

How successfully the agency walks this tightrope could well determine whether the recovery gathers force, or whether home prices slide again � perhaps creating a fresh economic downturn.

As recently as a few weeks ago, the F.H.A. had said that even under the bleakest economic forecast, its cash cushion would quickly recover. On Thursday, it abandoned that position.

�There is a real risk. Nobody has a crystal ball,� Shaun Donovan, secretary of housing and urban development, said in an interview. �We recognize there is a possibility that the reserves go below zero and stay there.�

Still, Mr. Donovan stressed that the agency, which had a role in one out of five home purchases in the last year, would not need a direct taxpayer bailout.

and why is that?

�There is no extraordinary action that Congress or anyone else needs to take,� he said during a news conference in Washington.

Instead, the agency would borrow from the Treasury, under authority previously granted by Congress.

Instead, the agency would borrow from the Treasury, under authority previously granted by Congress.

The F.H.A.�s annual audit was scheduled for release last week, but was mysteriously delayed at the last minute. On Thursday, as it released the document, the agency explained that it wanted its auditors to include more negative forecasts as a way of understanding the worst-case risk.

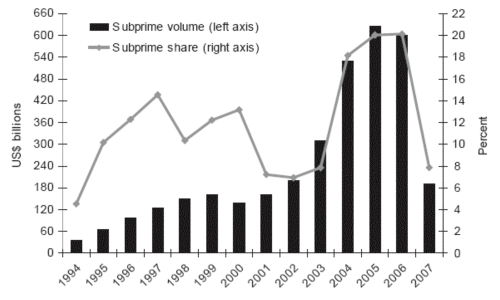

The audit showed reserves to be 0.53 percent of the total portfolio, far below the 2 percent minimum mandated by Congress and far less than the audit last year had forecast. In 2007, just before housing prices began their worst slump in decades, the reserves were above 6 percent.

Ann Schnare, a consultant who has analyzed the F.H.A. balance sheet, put the situation this way: �They�re running on empty.�

The audit showed reserves to be 0.53 percent of the total portfolio, far below the 2 percent minimum mandated by Congress and far less than the audit last year had forecast. In 2007, just before housing prices began their worst slump in decades, the reserves were above 6 percent.

Ann Schnare, a consultant who has analyzed the F.H.A. balance sheet, put the situation this way: �They�re running on empty.�

Nearly one in five loans it insured in 2007 falls into the category of �seriously delinquent,� it said Thursday. These loanholders are at least three months behind in their payments. For 2008 loans, 12 percent of them were seriously delinquent.

The F.H.A. says it is insuring loans to more financially secure buyers with higher credit scores. The average credit score of new borrowers, it said, is 693, compared with 633 two years ago.

In a sense, the agency is bulking up and giving as many loans as it can to qualified buyers as a way to diminish the relative size of the pool of problem loans. It guaranteed more than $360 billion in mortgages in the last year, four times the amount of 2007.

Critics say this is only increasing the size of the ultimate peril.

�They keep saying they�re going to outrun their problems, but some way, somehow, the taxpayer is going to end up on the hook,� said Edward Pinto, a former executive with Fannie Mae.

The F.H.A. says it is insuring loans to more financially secure buyers with higher credit scores. The average credit score of new borrowers, it said, is 693, compared with 633 two years ago.

In a sense, the agency is bulking up and giving as many loans as it can to qualified buyers as a way to diminish the relative size of the pool of problem loans. It guaranteed more than $360 billion in mortgages in the last year, four times the amount of 2007.

Critics say this is only increasing the size of the ultimate peril.

�They keep saying they�re going to outrun their problems, but some way, somehow, the taxpayer is going to end up on the hook,� said Edward Pinto, a former executive with Fannie Mae.

Brian Montgomery, who ran the F.H.A. for the Bush administration, said in a recent interview that the agency felt it had no choice but to open the doors to a broader group of applicants. Citing pressure from Congress and the White House, Mr. Montgomery said: �We had to let these loans through.�

Comment