Tweet

Tweet

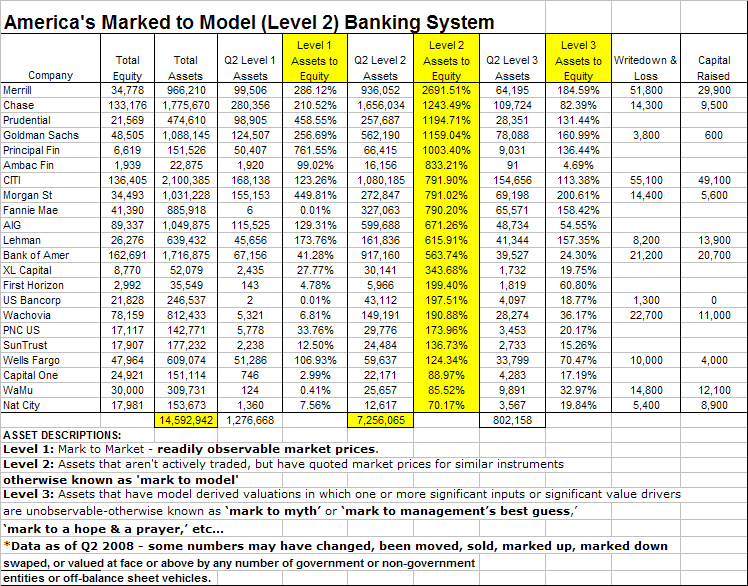

Re: "It Could Get Ugly Very Fast": Banking Crisis Grows, FDIC's Funds Shrink

The only prediction, other than iTulip, of a 1000 bank failures. That I've seen so far.

http://us1.institutionalriskanalytic...ry.asp?tag=378

Originally posted by metalman

View Post

http://us1.institutionalriskanalytic...ry.asp?tag=378

Comment