Tweet

Tweet

Re: The great bailout - Europe's best-kept secret

Not sure if you are refering to an earlier post I made on this topic - but here is David McWilliams explanation of the bailout (at least the mechanism as it pertains to Ireland) - Headline should read "ECB facilitates Irish Governments efforts to borrow the people of Ireland into financial oblivion")

http://www.davidmcwilliams.ie/2009/0...upport-machine

Ironically, it looks as if the Irish banks - and also, by virtue of these unusual circumstances, the Irish government - have just found an all-forgiving priest in the guise of the European Central Bank. The ECB is keeping us afloat. Back in January, on the Marian Finucane programme, I suggested that maybe the only thing we could do while we remained in EMU, was to threaten a default if the ECB didn’t support us by injecting liquidity into our financial system. Maybe the threat would not have to be explicit; just by looking at the desperation of our plight, the ECB would figure out that we needed serious help or else the country would go under, and deliver a huge blow to the credibility of the euro in the process.

Today, this is precisely what is happening. We have managed to shift the burden for much of the funding of the day today needs of this economy onto the ECB and, for this, our finance minister, Brian Lenihan, should be applauded. It’s not a long-term fix, but it is does give us short-term respite. More significantly, by using the ECB, Lenihan has managed to get the European Central Bank to print money for the Irish government, which breaks the first rule in the central bankers’ rulebook.

Given some of the ideologues at the ECB, that’s no mean feat. Not only that, but it surely breaks the most important stipulation of the Maastricht Treaty, which is that governments will never be financed by central banks.

Let’s have a look at how we are still breathing, and examine the rudiments of the ‘Lenihan life support machine’.

Furthermore, let’s speculate on how long we can get away with this, because there is no doubt that if the average German were fully aware of what was going on, he would freak out. His central bank was, yet again, funding what he would see as endemic Irish delinquency.

Until the liquidity crisis last September, if the Irish banks wanted money, they just issued their own paper in the market and borrowed cash. This wholesale money market financing allowed them to lend out huge amounts of cash and, as long as this market remained open to them, the Irish banks could keep rolling over their debts. At some stage, this would implode, but the view in the boardrooms was very much one of ‘‘let’s ride this thing while we can, and let someone else worry about tomorrow’’.

But tomorrow came rather quickly and suddenly after the end of Lehman Brothers and the market shut down. The Irish banks were looking at a massive funding crisis and an acute liquidity collapse leading to insolvency. If a bank can’t get money, it’s not a bank.

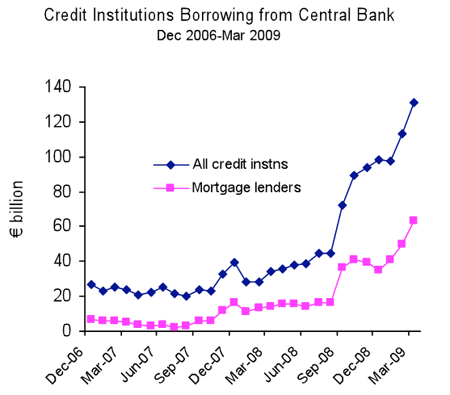

As you can see from the chart on the left (taken from a paper given by Professor Patrick Honohan of Trinity College last week, which can be read at www.irisheconomy.ie), the banks turned to the Central Bank for money. Before the crisis, the banks were depending on the ECB for about €30 billion in short-term finance. Today, that figure is a whopping €140 billion.

As the lender of last resort, the Central bank is obliged to give the banks money.

But the amount has increased so dramatically that now the Central Bank is no longer the lender of last resort; it is in many cases, the only lender of any resort. The Central Bank gets all its cash from the ECB, so the ECB has turned into the Irish bank’s lifeline.

But this is not where the story ends; here is where it gets interesting, because the ECB is accepting Irish government stock as collateral from the banks to release this cash. The Irish banks are buying Irish government bonds and then cashing them in for euro at the ECB’s discount window.

So, while ensuring that the banking system can continue to tick over, the Irish government is using the Irish banks as a proxy in order to get the ECB to fund our budget deficit.

Now, this is interesting and clever - in a smart-arsed kind of way. The Irish government issues bonds to pay for the dole here, and for public sector pay and services and all the other things it must pay for. The banks buy some of these bonds for cash - the rest are bought by other Irish and international investors. The state gets the cash and gives it to us. Then the Irish banks can go to the ECB and get cash, and this facilitates whatever credit they are extending. Probably more significantly, the banks are using this credit to keep builders from going bust by rolling up interest payments.

The government insists that it is not leaning on the banks to buy Irish government bonds. And it is true that, as market conditions have settled a little in recent weeks and the government has gone on the offensive internationally, a wider spread of investors has started to go back into the market for our bonds.

However, the reality is that the ECB carrot is there in front of the banks’ noses - and Dr Michael Somers, the NTMA chief, referred to this in his recent evidence to the D�il Public Accounts Committee, when he said he suspected that banks were using bonds to access cash from the ECB.

What’s more, the bonds the banks will get from the state in return from assets transferred to the new National Asset Management Agency (Nama) will also be usable as collateral to access cash from the ECB. Senior officials, including Somers, held discussions with ECB president JeanClaude Trichet before the Nama announcement and this was, presumably, one of the key issues covered. This will provide further funding for the banks and means the ECB will effectively support the funding of the clean-up plan.

Is it sustainable? Can we just carry on like this? Perhaps not, if the average German gets wind of what’s happening.

Our Minister for Finance will know that his key job in the months ahead will be to develop a banking system which can stand on its own two feet and again start to access funding on a normal basis from the markets.

If confidence can be restored, the banks can start raising cash again from the markets, paying down the state redeemable preference shares, and returning to normal operations. But we are still a long, long way from there. In the meantime, we need our friends in Frankfurt.

Originally posted by FrankL

View Post

http://www.davidmcwilliams.ie/2009/0...upport-machine

Ironically, it looks as if the Irish banks - and also, by virtue of these unusual circumstances, the Irish government - have just found an all-forgiving priest in the guise of the European Central Bank. The ECB is keeping us afloat. Back in January, on the Marian Finucane programme, I suggested that maybe the only thing we could do while we remained in EMU, was to threaten a default if the ECB didn’t support us by injecting liquidity into our financial system. Maybe the threat would not have to be explicit; just by looking at the desperation of our plight, the ECB would figure out that we needed serious help or else the country would go under, and deliver a huge blow to the credibility of the euro in the process.

Today, this is precisely what is happening. We have managed to shift the burden for much of the funding of the day today needs of this economy onto the ECB and, for this, our finance minister, Brian Lenihan, should be applauded. It’s not a long-term fix, but it is does give us short-term respite. More significantly, by using the ECB, Lenihan has managed to get the European Central Bank to print money for the Irish government, which breaks the first rule in the central bankers’ rulebook.

Given some of the ideologues at the ECB, that’s no mean feat. Not only that, but it surely breaks the most important stipulation of the Maastricht Treaty, which is that governments will never be financed by central banks.

Let’s have a look at how we are still breathing, and examine the rudiments of the ‘Lenihan life support machine’.

Furthermore, let’s speculate on how long we can get away with this, because there is no doubt that if the average German were fully aware of what was going on, he would freak out. His central bank was, yet again, funding what he would see as endemic Irish delinquency.

Until the liquidity crisis last September, if the Irish banks wanted money, they just issued their own paper in the market and borrowed cash. This wholesale money market financing allowed them to lend out huge amounts of cash and, as long as this market remained open to them, the Irish banks could keep rolling over their debts. At some stage, this would implode, but the view in the boardrooms was very much one of ‘‘let’s ride this thing while we can, and let someone else worry about tomorrow’’.

But tomorrow came rather quickly and suddenly after the end of Lehman Brothers and the market shut down. The Irish banks were looking at a massive funding crisis and an acute liquidity collapse leading to insolvency. If a bank can’t get money, it’s not a bank.

As you can see from the chart on the left (taken from a paper given by Professor Patrick Honohan of Trinity College last week, which can be read at www.irisheconomy.ie), the banks turned to the Central Bank for money. Before the crisis, the banks were depending on the ECB for about €30 billion in short-term finance. Today, that figure is a whopping €140 billion.

As the lender of last resort, the Central bank is obliged to give the banks money.

But the amount has increased so dramatically that now the Central Bank is no longer the lender of last resort; it is in many cases, the only lender of any resort. The Central Bank gets all its cash from the ECB, so the ECB has turned into the Irish bank’s lifeline.

But this is not where the story ends; here is where it gets interesting, because the ECB is accepting Irish government stock as collateral from the banks to release this cash. The Irish banks are buying Irish government bonds and then cashing them in for euro at the ECB’s discount window.

So, while ensuring that the banking system can continue to tick over, the Irish government is using the Irish banks as a proxy in order to get the ECB to fund our budget deficit.

Now, this is interesting and clever - in a smart-arsed kind of way. The Irish government issues bonds to pay for the dole here, and for public sector pay and services and all the other things it must pay for. The banks buy some of these bonds for cash - the rest are bought by other Irish and international investors. The state gets the cash and gives it to us. Then the Irish banks can go to the ECB and get cash, and this facilitates whatever credit they are extending. Probably more significantly, the banks are using this credit to keep builders from going bust by rolling up interest payments.

The government insists that it is not leaning on the banks to buy Irish government bonds. And it is true that, as market conditions have settled a little in recent weeks and the government has gone on the offensive internationally, a wider spread of investors has started to go back into the market for our bonds.

However, the reality is that the ECB carrot is there in front of the banks’ noses - and Dr Michael Somers, the NTMA chief, referred to this in his recent evidence to the D�il Public Accounts Committee, when he said he suspected that banks were using bonds to access cash from the ECB.

What’s more, the bonds the banks will get from the state in return from assets transferred to the new National Asset Management Agency (Nama) will also be usable as collateral to access cash from the ECB. Senior officials, including Somers, held discussions with ECB president JeanClaude Trichet before the Nama announcement and this was, presumably, one of the key issues covered. This will provide further funding for the banks and means the ECB will effectively support the funding of the clean-up plan.

Is it sustainable? Can we just carry on like this? Perhaps not, if the average German gets wind of what’s happening.

Our Minister for Finance will know that his key job in the months ahead will be to develop a banking system which can stand on its own two feet and again start to access funding on a normal basis from the markets.

If confidence can be restored, the banks can start raising cash again from the markets, paying down the state redeemable preference shares, and returning to normal operations. But we are still a long, long way from there. In the meantime, we need our friends in Frankfurt.

Comment