Tweet

Tweet

Shadow inventory is still very much a part of the housing market. This inventory is slowly making its way through the system. Once the home is on the market for sale, it is no longer in the shadows. With constrained inventory and interest rates providing a boost to the leverage a buyer can take on, banks are slowly leaking out more of these properties for your viewing consumption. People have asked how is it that so many people can be living in homes without making a payment. Shadow inventory is simply a modern day oddity of this housing market. In any other typical housing market you would see inventory increasing either through new building or people putting homes for sale given the uptick in home values. Yet millions of Americans, over 10 million cannot sell because they are underwater. Over 4 million are deep in distress. Speculation about the shadow inventory draw down for 2013 is already coming out.

Shadow inventory draw down for 2013

According to LPS and their latest Mortgage Monitor Report 5,300,000 are in some stage of distress:

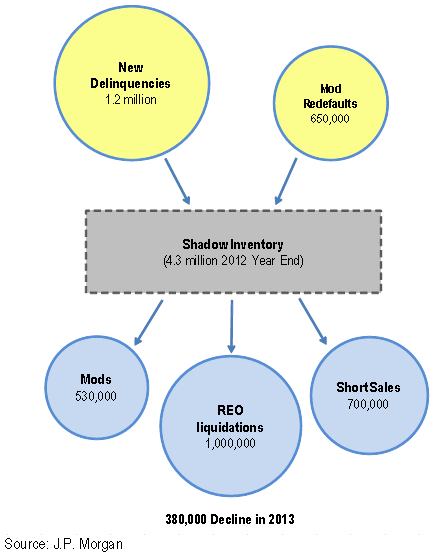

Depending on the definition of shadow inventory, the number can be lower. Typically the number is based on the number of properties not on the MLS but are in some stage of distress. According to JP Morgan this number is up to 4,300,000 at the end of this year. Their projections for 2013 shadow inventory is telling:

The above is an interesting breakdown. JP Morgan is expecting 1.2 million new foreclosures and 650,000 loan modifications that will re-default. Given the horrible loans in FHA products this should come as no surprise. The numbers then include another 530,000 new mods, 1 million foreclosure sales, and 700,000 short sales. By the end of 2013 we should see the shadow inventory decline by 380,000 leaving us still with about 4 million properties. So much for the non-existent shadow inventory.

I would also like to point out the incredibly high number of new delinquencies. These tell more of the story. Why are we still seeing an incredibly high number of foreclosures in a recovering economy? The problem of course is that household incomes are not going up and households are still being strained on the income front. Having 1.2 million foreclosures in 2013 isn�t exactly an optimistic forecast. And take a look at those 650,000 mod re-defaults. This is simply more prolonging the inevitable for many home owners but someone is paying for this. Those paying for this are those currently buying at inflated prices and also those seeing their buying power decrease via Federal Reserve actions. Ironically the hike in rents is hitting those least likely in our society to afford it. The CPI isn�t really a good measure because many of the hidden cost are being passed on via debt based products like higher education and purchasing homes that gain a boost with lower rates.

Household formation

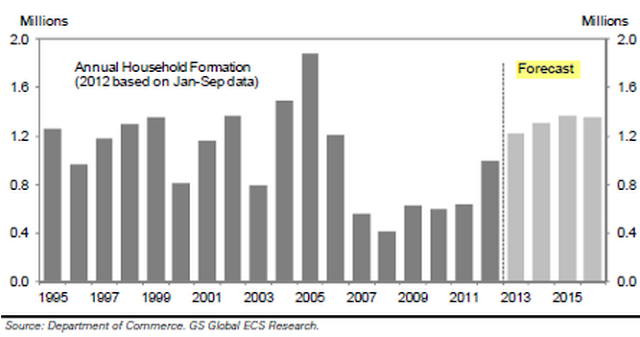

Household formation has been weak since the recession hit. In more typical years the US adds about 1.2 million new households. This can come in the form of renters or buyers:

Source: GS

(this chart clearly shows the societal implications of the bubble and its collapse - new household formation surges, then nose dives)

The projections are for 1.2 million new households. There are a couple of reasons why we will have to wait and see if this will play out. First, younger Americans are typically the first to go out and form households. There are very little indications that they are doing well. Many are saddled with enormous amounts of student debt already. A large portion are working in jobs that pay very little plus many are underemployed. Household formation will occur when this group undergoes a strong growth in their earnings potential.

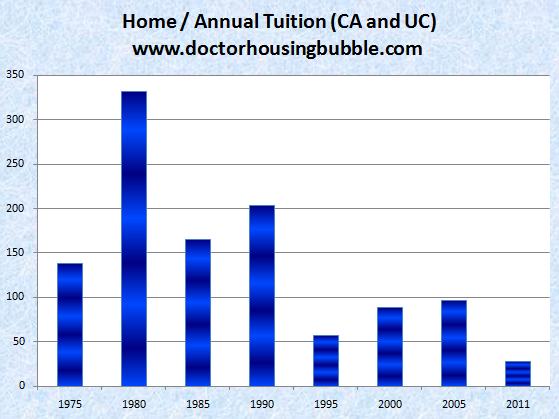

In California, we did a comparison between the University of California tuition and home prices in the state:

�This is an interesting perspective. The cost of an UC degree was cheapest in 1980 in relation to housing prices. For example, for the cost of the median home in California in 1980 you would have been able to purchase over 330 years of education at the UC. Today the cost of a median priced California home will only get you 22 years of college education.�

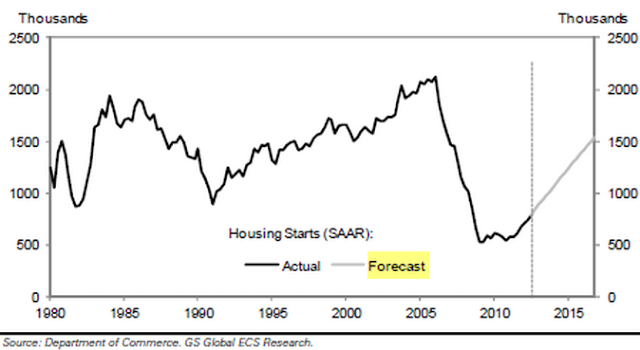

This goes back to the point that younger Americans are paying a much higher cost for education than the previous generation. The draw down in shadow inventory will largely depend on how well the economy recovers for this group. Housing starts are still low but did move up this year and projections are pushing this figure much higher next year:

With the fiscal issues hitting the country next year we will have to keep an eye on the underlying household income growth and employment prospects for many to determine whether the housing market will improve. This year the big boost has come from the Fed and constrained housing inventory. Investors have also jumped in to eat up a large portion of supply (about 1 out of every 3 purchases). Builders have not gone out in full force because they fully understand that cash strapped Americans are looking for cheaper properties (that is based on the monthly payment) and not more expensive newer homes. The shadow inventory is going to be part of this housing market for years to come.

http://www.doctorhousingbubble.com/s...ld-formations/

Shadow inventory draw down for 2013

According to LPS and their latest Mortgage Monitor Report 5,300,000 are in some stage of distress:

-1,957,000 late 30 days or more, but less than 90 days

-1,543,000 90 or more days late, but not in foreclosure

-1,800,000 in foreclosure process

-1,543,000 90 or more days late, but not in foreclosure

-1,800,000 in foreclosure process

Depending on the definition of shadow inventory, the number can be lower. Typically the number is based on the number of properties not on the MLS but are in some stage of distress. According to JP Morgan this number is up to 4,300,000 at the end of this year. Their projections for 2013 shadow inventory is telling:

The above is an interesting breakdown. JP Morgan is expecting 1.2 million new foreclosures and 650,000 loan modifications that will re-default. Given the horrible loans in FHA products this should come as no surprise. The numbers then include another 530,000 new mods, 1 million foreclosure sales, and 700,000 short sales. By the end of 2013 we should see the shadow inventory decline by 380,000 leaving us still with about 4 million properties. So much for the non-existent shadow inventory.

I would also like to point out the incredibly high number of new delinquencies. These tell more of the story. Why are we still seeing an incredibly high number of foreclosures in a recovering economy? The problem of course is that household incomes are not going up and households are still being strained on the income front. Having 1.2 million foreclosures in 2013 isn�t exactly an optimistic forecast. And take a look at those 650,000 mod re-defaults. This is simply more prolonging the inevitable for many home owners but someone is paying for this. Those paying for this are those currently buying at inflated prices and also those seeing their buying power decrease via Federal Reserve actions. Ironically the hike in rents is hitting those least likely in our society to afford it. The CPI isn�t really a good measure because many of the hidden cost are being passed on via debt based products like higher education and purchasing homes that gain a boost with lower rates.

Household formation

Household formation has been weak since the recession hit. In more typical years the US adds about 1.2 million new households. This can come in the form of renters or buyers:

Source: GS

(this chart clearly shows the societal implications of the bubble and its collapse - new household formation surges, then nose dives)

The projections are for 1.2 million new households. There are a couple of reasons why we will have to wait and see if this will play out. First, younger Americans are typically the first to go out and form households. There are very little indications that they are doing well. Many are saddled with enormous amounts of student debt already. A large portion are working in jobs that pay very little plus many are underemployed. Household formation will occur when this group undergoes a strong growth in their earnings potential.

In California, we did a comparison between the University of California tuition and home prices in the state:

�This is an interesting perspective. The cost of an UC degree was cheapest in 1980 in relation to housing prices. For example, for the cost of the median home in California in 1980 you would have been able to purchase over 330 years of education at the UC. Today the cost of a median priced California home will only get you 22 years of college education.�

This goes back to the point that younger Americans are paying a much higher cost for education than the previous generation. The draw down in shadow inventory will largely depend on how well the economy recovers for this group. Housing starts are still low but did move up this year and projections are pushing this figure much higher next year:

With the fiscal issues hitting the country next year we will have to keep an eye on the underlying household income growth and employment prospects for many to determine whether the housing market will improve. This year the big boost has come from the Fed and constrained housing inventory. Investors have also jumped in to eat up a large portion of supply (about 1 out of every 3 purchases). Builders have not gone out in full force because they fully understand that cash strapped Americans are looking for cheaper properties (that is based on the monthly payment) and not more expensive newer homes. The shadow inventory is going to be part of this housing market for years to come.

http://www.doctorhousingbubble.com/s...ld-formations/